A Large LINK Wallet Moves Ahead of ETF Speculation: Reading the On-Chain Clues

Every time a major digital asset edges closer to an exchange-traded fund, markets become hypersensitive to the smallest hint of positioning. Order-book snapshots, funding data and wallet trackers are all put under the microscope. That is exactly what is happening now around Chainlink (LINK).

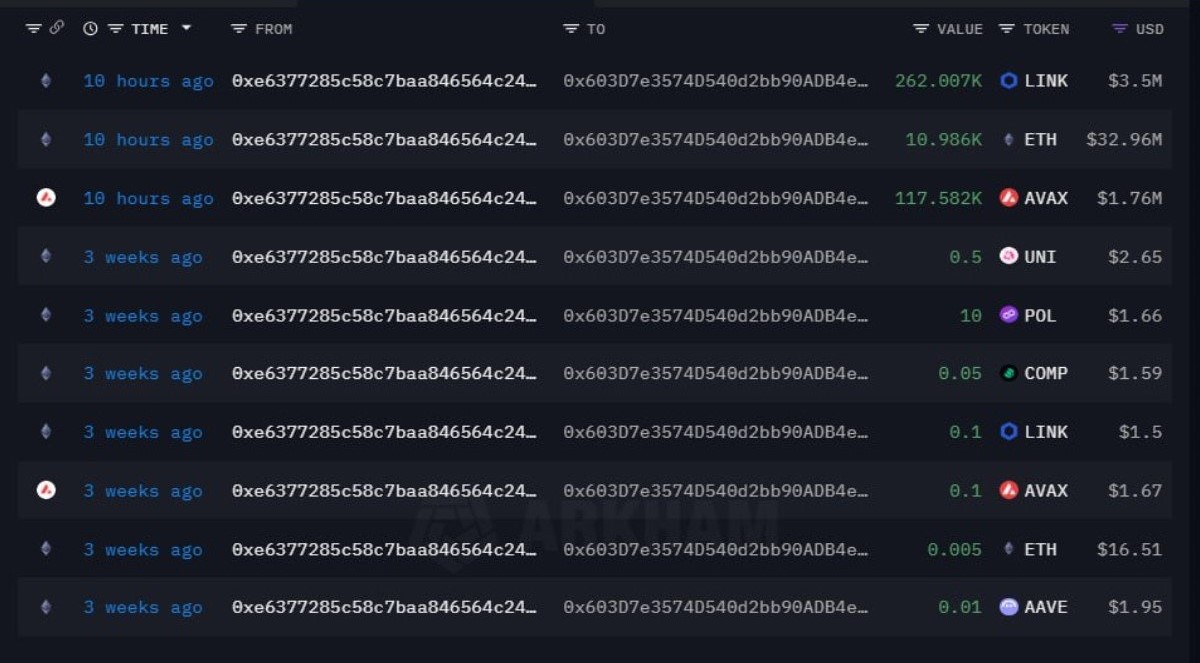

Roughly ten hours before this article was drafted, on-chain monitors flagged a notable sequence of transfers. A wallet that had been quietly accumulating LINK throughout 2025 moved about 262,007 LINK—worth roughly $3.5 million at current prices—to a newly created address. Within the same operation, the holder also shifted 10,986 ETH (about $33 million) and 117,582 AVAX (around $1.76 million) into the same destination.

In isolation, this could be dismissed as routine housekeeping. But there are two reasons the move has captured attention. First, the sending wallet has been linked by analysts to accumulation patterns often associated with professional liquidity providers such as Flow Traders and Cumberland. Second, the consolidation arrives just as discussion around a possible Chainlink ETF reaches a new crescendo, with filings and speculation about how an eventual product might source its underlying exposure.

The temptation is to reduce the story to a single narrative: "whale moves funds ahead of ETF, therefore a major price move is coming." Reality, as usual, is more complex. The goal of this article is not to declare a definitive motive, but to use the event as a case study in how to read on-chain data responsibly, especially when the word "ETF" is in the air.

1. The Transfers: What We Actually Know

Let us start with the facts that can be verified on-chain.

- Sending address:

0xe6377285c58c7baa846564c246d9dBe910398779 - Receiving address:

0x603D7e3574D540d2bb90ADB4eD03F3f6488e1962

From public blockchain data, we can observe the following flows into the new address:

- Approximately 262,007 LINK, aggregated in a series of transactions, worth around $3.5 million at current levels.

- Approximately 10,986 ETH, representing about $32.9 million.

- Approximately 117,582 AVAX, roughly $1.76 million.

Analysts tracking this wallet report that the outgoing address built these positions between January and August 2025. During that period, LINK, ETH and AVAX all experienced extended sideways ranges punctuated by bursts of volatility. In the case of LINK, most of the accumulation appears to have occurred during a large consolidation zone—precisely the kind of environment in which professional trading firms can quietly absorb liquidity from shorter-term participants.

Based on historical prices, the wallet’s average entry for LINK seems higher than today’s quotation, implying an unrealised loss. The ETH and AVAX tranches look closer to break-even or modestly profitable, depending on the exact acquisition dates. Importantly, the move to a new address does not by itself reveal whether the owner intends to hold, distribute, post collateral, or prepare inventory for institutional partners. All we can say with certainty is that a large multi-asset portfolio was deliberately consolidated.

2. Who Might Be Behind the Wallet?

Some researchers have suggested that the pattern of activity—size, timing, and overlap with known exchange and institutional routes—resembles the behaviour of market-making firms such as Flow Traders or Cumberland. These companies specialise in providing liquidity across venues and products. They are active in spot markets, derivatives, and increasingly in products that bridge traditional finance with digital assets.

It is crucial to stress that such attributions are probabilistic, not definitive. On-chain heuristics can cluster addresses that interact with the same counterparties or exhibit similar flow patterns, but they rarely provide absolute certainty about the real-world entity behind a wallet. In addition, professional firms often operate multiple layers of custody—internal sub-accounts, third-party custodians and segregated addresses for different strategies or clients.

With that caveat, the hypothesis of a professional liquidity provider is at least consistent with three observable facts:

- The wallet holds a basket of large-cap assets—LINK, ETH and AVAX—rather than a single highly speculative token.

- The accumulation window spans months of quiet trading, suggesting a methodical build-up rather than impulsive participation in short-term excitement.

- The consolidation into a fresh address occurs at a moment when institutional interest in Chainlink-related products is intensifying, including talk of ETF launches.

Even if we cannot name the entity with certainty, treating the wallet as representative of professional money management helps frame the analysis. It invites questions such as: How would a firm that provides liquidity for an ETF structure its inventory? What role might a multi-asset basket play? And how do unrealised losses factor into those decisions?

3. Why Move Now? A Tour of Plausible Motives

On-chain data rarely gives us motives; it gives us patterns. To interpret them, we need to think in terms of scenarios rather than conclusions. Here are several possibilities that fit the observed transfers.

3.1 Operational Reorganisation and Risk Segregation

One straightforward explanation is that the owner is reorganising custody. Professional trading desks often separate exposure into different buckets: proprietary positions, client balances, hedging inventory, and reserves for specific venues. Moving a large, mixed portfolio into a new address could simply reflect a desire to segregate assets earmarked for a particular use—for example, to support future structured products or to keep collateral for certain agreements distinct from day-to-day trading inventory.

From a risk-management perspective, consolidating assets into a fresh wallet can also make monitoring and auditing easier. If the address is linked to a custodian or to internal treasury operations rather than an active trading book, it might see fewer outbound transactions but more interactions with institutional partners over time.

3.2 Preparing Inventory for ETF-Related Activity

Another widely discussed scenario is that the move relates to potential ETF activity around Chainlink. In a typical ETF structure, authorised participants (APs) create and redeem shares by delivering or receiving the underlying asset in large blocks. These operations often involve specialist liquidity providers who can source and warehouse the asset efficiently.

If an ETF tied to Chainlink is indeed approaching launch, professional desks might choose to consolidate LINK holdings into addresses designated for that purpose. Bundling ETH and AVAX into the same wallet could serve multiple functions:

- ETH may be used for transaction fees, collateral in derivatives markets, or as part of cross-asset hedging strategies that offset short-term movements in LINK.

- AVAX, as another major network token, might form part of a broader cross-chain liquidity portfolio that supports baskets, structured notes or pairs offered to institutional clients.

None of this proves that the specific wallet will be involved in ETF operations, but the timing and composition of the move align with how multi-asset liquidity desks often prepare for new product launches in traditional finance.

3.3 Managing Unrealised Losses Without Closing Exposure

The observation that the wallet appears to be underwater on its LINK position adds an interesting twist. If the owner were simply looking to exit, we would expect to see transfers from the wallet to exchanges and a reduction in balances, not a consolidation into a new address. Instead, the move suggests a willingness to continue holding LINK despite short-term mark-to-market losses.

There are several reasons a professional firm might act this way:

- They may have hedged directional risk elsewhere, so the spot position is part of a larger strategy whose success does not depend on immediate price appreciation.

- They may view LINK as a strategic asset within the infrastructure stack, with a horizon measured in years rather than weeks, making interim losses tolerable.

- They may anticipate that a new ETF or related institutional products will eventually generate sufficient demand to justify maintaining a large inventory even through adverse price swings.

In each of these cases, shifting the tokens into a dedicated wallet could signal a transition from an “accumulation and trading” phase to a “hold and deploy when needed” phase.

3.4 Staging for Over-the-Counter Arrangements

A final, more technical possibility is that the wallet is being prepared for over-the-counter (OTC) transactions with institutional partners. Rather than executing large orders directly on exchanges—where they could move prices and create slippage—big players often negotiate block trades privately and settle on-chain. A clean, newly funded wallet is easier to reference in contracts and compliance reviews than an address with years of mixed activity.

If an asset manager, corporate treasury or ETF sponsor were seeking a substantial quantity of LINK, ETH or AVAX, a liquidity provider might stage inventory in a segregated wallet before settlement. Again, on-chain data alone cannot confirm that this is happening, but the pattern is compatible with common OTC practices in both digital and traditional markets.

4. How Could an ETF Influence LINK’s Market Dynamics?

Even if the wallet move is unrelated to ETF developments, the question remains: how might ETF flows shape LINK’s trajectory over time? Here it helps to step back from individual addresses and consider the mechanics of these products.

4.1 Creation, Redemption and the Role of Liquidity Providers

When an ETF is launched, authorised participants can create new shares by delivering the underlying asset (in this case, LINK) to the fund’s custodian. They receive ETF shares in return, which they can then sell on an exchange. The reverse process—redemption—occurs when APs deliver ETF shares back to the fund and receive the underlying asset.

In steady state, this process keeps the ETF’s price close to the value of its holdings. If ETF shares trade at a premium, APs can deliver LINK to the fund, receive shares, and sell them, nudging the price back toward net asset value. If shares trade at a discount, APs can buy them, redeem for LINK and sell the tokens, again helping align prices.

Professional liquidity providers sit at the center of this process. They need access to substantial spot inventory and to derivatives that help them manage short-term price risk. The wallet we are analysing could be one piece of that puzzle—a pool of LINK, ETH and AVAX organised to support such operations.

4.2 ETF Flows Are Not One-Way

It is important, however, to resist the idea that an ETF guarantees a continuous stream of net buying. Flows can be positive or negative depending on investor demand. In the early days of a new product, there may be bursts of creation as asset managers add exposure, followed by quieter periods or even net redemptions if sentiment shifts.

For LINK, an ETF could change who owns the asset and how long they hold it more than it changes the long-term supply trajectory. Some investors who previously avoided self-custody may finally choose to gain exposure through a regulated fund. Others who already hold LINK directly might rebalance by shifting part of their position into ETF shares for convenience. Over time, this can increase liquidity and potentially reduce frictions around rebalancing, but the directional impact on price will still depend on whether aggregate demand rises or falls.

4.3 Second-Order Effects: Volatility, Correlations and Narrative

Beyond direct flows, ETFs can also affect an asset’s behaviour indirectly:

• Volatility patterns. Wider participation through traditional brokerages can change the rhythm of trading, with more emphasis on standard market hours and index-driven flows.

• Correlation with other assets. If LINK becomes part of diversified digital-asset or infrastructure baskets, its price may move more in sync with other large tokens or even with equity sectors sensitive to similar themes.

• Narrative reinforcement. The very existence of an ETF signals that an asset has reached a certain level of maturity and institutional acceptance. For Chainlink, which already plays a key role in oracle infrastructure, this could further cement its status as part of the core plumbing of the crypto-native financial stack.

Large holders like the wallet we are analysing may be positioning not only for immediate flows, but also for these second-order shifts in how the market perceives and uses LINK.

5. A Framework for Interpreting Large Wallet Moves

Given the excitement around ETF narratives, it is easy to overreact to a single wallet move. To keep analysis grounded, it can help to adopt a simple framework whenever a similar event appears on dashboards.

1. Separate facts from stories. Facts: a specific amount of LINK, ETH and AVAX moved from one address to another at a known time. Stories: who owns the wallet, what their strategy is, and how the transfer relates to future events. Keeping these categories distinct prevents speculation from hardening into pseudo-certainty.

2. Consider multiple motives. Operational reorganisation, preparation for institutional products, OTC staging, and long-term treasury management are all viable explanations. The truth may even be a combination of them.

3. Watch for follow-through. If the new address begins interacting with custodians, ETF administrators or major OTC counterparties, that will strengthen certain hypotheses. If it sits idle, the move may have been primarily for internal housekeeping.

4. Contextualise with broader data. Exchange balances, derivatives positioning, and activity from other large LINK holders can confirm whether this transfer is part of a larger pattern or a one-off event.

Most importantly, it is wise to remember that on-chain data is descriptive, not prescriptive. It tells us what has happened, not what must happen next.

6. Conclusion: Signals, Not Certainties

The consolidation of roughly 262,000 LINK, nearly 11,000 ETH and over 117,000 AVAX into a fresh wallet would be noteworthy at any time. Coming just as the market focuses on a potential Chainlink ETF, it naturally invites deeper scrutiny.

The evidence suggests that a sophisticated holder—possibly a professional liquidity provider—has chosen to organise its positions in a way that could support institutional activity around LINK and related assets. The presence of unrealised losses in LINK does not contradict this; if anything, it highlights that long-horizon strategies can tolerate interim drawdowns when they are built around infrastructure themes rather than short-term excitement.

Still, the move is better understood as a signal about positioning and structure than as a guarantee of how prices will evolve. An ETF can change who holds LINK and how they access it, but the balance of supply and demand will continue to be shaped by usage, macro conditions and the pace at which real-world applications adopt Chainlink’s oracle infrastructure.

For observers, the most productive response may be curiosity rather than certainty: track the wallet’s future interactions, study how ETF mechanics intersect with on-chain liquidity, and treat each new data point as part of a mosaic rather than a crystal ball.

This article is intended solely for informational and educational purposes. It does not constitute financial, investment, legal or tax advice, and it is not a recommendation to buy, sell or hold LINK, ETH, AVAX or any other digital asset. Digital assets are volatile and can involve significant risk of loss. Readers should conduct their own research and consider consulting qualified professionals before making decisions related to digital assets or other investments.