Could Strategy Ever Sell Its Bitcoin? Reading the CEO’s 'Last Resort' Comment

Strategy has built its entire identity around one simple idea: Bitcoin is the primary treasury asset, and the company will keep accumulating it for the very long term. For years, the message from leadership seemed absolute. The firm repeatedly stated that it would never sell BTC, only acquire more, even as the price moved above 100,000 USD.

That clear narrative made Strategy a symbol. To many investors, it was the purest expression of a listed company committing itself to the Bitcoin standard. When the company raised debt or issued new equity, the proceeds largely went into additional BTC purchases. Supporters viewed it as a leveraged bet on digital scarcity; critics saw it as an aggressive balance-sheet experiment.

Now the conversation has become more nuanced. In a 29 November 2025 appearance on the What Bitcoin Did podcast, CEO Phong Le added an important qualifier. He explained that while the company still treats Bitcoin as its core holding, it could sell BTC if doing so were necessary to protect shareholders in a specific scenario: when the stock trades below one times modified net asset value (mNAV) and the firm needs cash to fund dividends.

His line that caught everyone’s attention was simple: Strategy 'can sell Bitcoin, and we will sell if needed to fund dividends when the stock trades below 1x mNAV'. He was careful to emphasise that this is a last resort, not a reversal of the long-term strategy. Even so, markets reacted quickly. The company’s share price fell double digits intraday on 1 December before closing down around 3.3%, and Bitcoin briefly slipped below 85,000 USD.

Is this the beginning of a structural shift, or simply a reminder that even the most committed corporate holder has constraints? To answer that, we need to unpack three pieces: what mNAV actually measures, what Strategy’s balance sheet looks like today, and how different price paths for BTC change the pressure on management.

1. What Exactly Did the CEO Say?

First, it is important to separate the headline from the full context. On the podcast, Phong Le reiterated several familiar points:

- Bitcoin remains the company’s primary treasury asset and long-term focus.

- The firm has consistently accumulated BTC since 2020 and continues to view it as a strategic reserve.

- The leadership still believes that over a multi-decade horizon, Bitcoin can outperform traditional stores of value.

The new nuance came when the host asked about dividends, leverage and shareholder obligations. Le responded that Strategy has a responsibility to all stakeholders, not only to those who prioritise Bitcoin exposure above everything else. If the company’s stock trades below its modified net asset value (mNAV) and other funding avenues are closed, selling a portion of the BTC stack to fund dividends could be considered.

Two elements matter here:

- Conditional language. The phrase 'we can sell, and we will sell if needed' is anchored to a scenario where mNAV falls below 1x and stays there, and where other financing tools are not available on reasonable terms.

- Positioning as last resort. Le framed BTC sales as a final option, after the company has already drawn down cash reserves, explored equity issuance, refinanced debt where possible and adjusted dividend policies.

This is not the first time Strategy has acknowledged the possibility. In April 2025, the firm’s regulatory filing already flagged a scenario in which it might sell BTC in 2026 if the price dropped significantly and servicing obligations in dollars became difficult. The podcast did not create this risk; it simply brought it into the public conversation in more direct language.

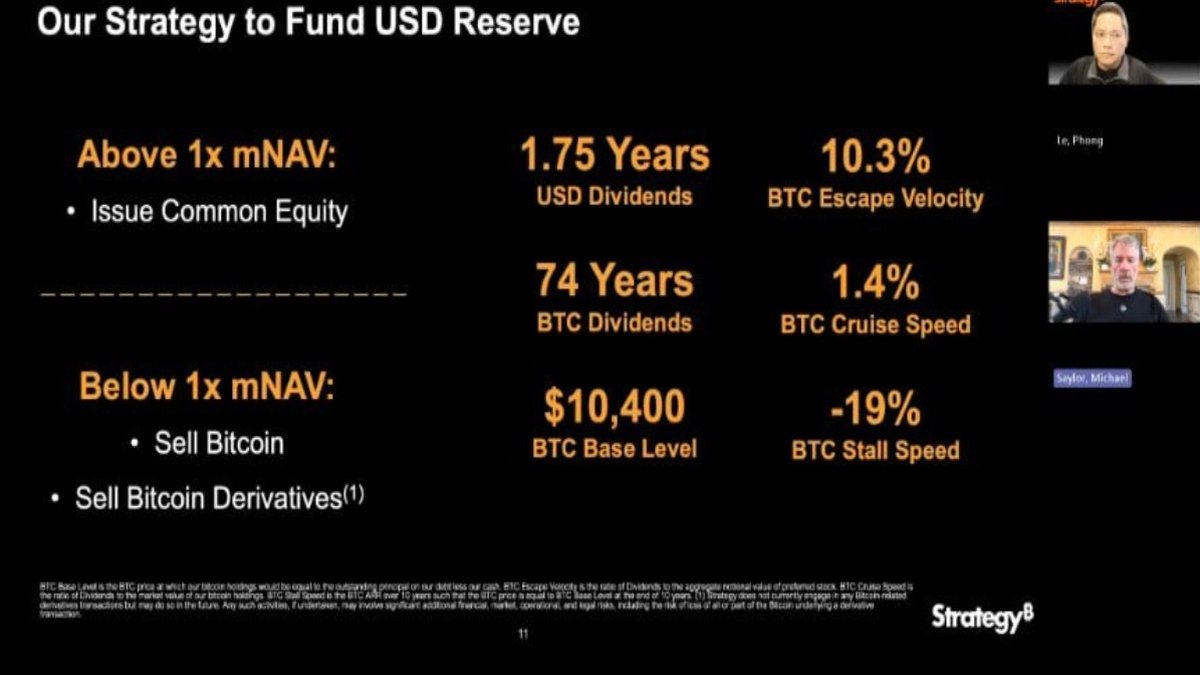

2. A Quick Primer on mNAV: Why 1x Matters

To understand why mNAV has become the focal point, we need to look at how a company like Strategy is valued.

At a high level, modified net asset value (mNAV) compares the market capitalisation of the company with the value of its underlying Bitcoin holdings and other net assets. A simplified version looks like this:

mNAV = Market capitalisation of Strategy / (Value of BTC holdings + other assets − debt)

In practice, analysts adjust for various items, but the intuition is straightforward:

- mNAV > 1x means the equity market is willing to pay a premium over the net value of the BTC plus other assets on the balance sheet. Investors are effectively valuing the company’s strategy, brand, trading liquidity and optionality.

- mNAV < 1x means the market capitalisation is lower than the estimated net value of the assets. In other words, the company trades at a discount to the BTC it holds.

For a firm whose strategy is to raise capital and convert it into Bitcoin, this ratio is crucial. When mNAV is comfortably above 1x, issuing new shares to buy more BTC can be seen as accretive. The company is raising funds at a valuation that exceeds the per-share value of its holdings. When mNAV falls below 1x for an extended period, that mechanism breaks down. Issuing equity at a discount becomes unattractive because it dilutes existing shareholders without clearly increasing their claim on BTC.

That is why the CEO points to mNAV < 1x as a stress scenario. If the company cannot raise funds efficiently through equity, and if debt markets are not receptive, then the main remaining source of liquidity is the very BTC it holds.

3. The Balance Sheet Today: Cash, Debt and Custody

Against that backdrop, the company has taken steps to reduce near-term pressure:

• Cash reserve: Strategy recently disclosed that it holds approximately 1.44 billion USD in cash, raised primarily through share sales. According to management, this gives the company an estimated 21–23 months of coverage for dividends and interest payments, even without selling any Bitcoin.

• Diversified custody: The firm is also transferring a portion of its BTC holdings into custody with Fidelity. This move is framed as a way to increase transparency and reassure both shareholders and regulators that the assets backing the strategy are professionally safeguarded.

• Ongoing accumulation: Despite recent volatility, the company has continued to purchase BTC when conditions allow, extending a buying streak that began in 2020.

These elements matter because they define the 'runway' before any last-resort sale becomes a serious possibility. With nearly two years of operating coverage and no immediate debt maturity crisis, the company emphasises that it does not expect to sell BTC in the near term under its base case.

4. Why Markets Reacted Anyway

If the probability of an imminent sale is low, why did the stock and Bitcoin both drop after the podcast?

Part of the answer lies in narrative. For several years, Strategy’s message was simple and powerful: 'We will never sell.' That statement turned the company into a symbol of extreme conviction, and many investors used it as a mental anchor when thinking about a potential floor under Bitcoin demand. When the same leadership later says 'we could sell under specific conditions', even if those conditions are remote, it disrupts that story.

Markets tend to react not only to new information, but to changes in perceived certainty. The shift from 'never' to 'only as a last resort' may be rational and responsible from a corporate governance viewpoint, yet it still feels like a downgrade in commitment. Some holders respond by de-risking, others by reassessing their assumptions about how much downside protection Strategy really provides to the BTC market.

There is also a mechanical element. The company’s equity (traded as MSTR) is a popular vehicle for investors who want Bitcoin exposure but prefer traditional brokerage accounts. When that stock sells off, some algorithmic strategies and discretionary funds may reduce BTC holdings at the same time, reinforcing short-term moves. On 1 December, this interplay coincided with a broader risk-off tone, helping push Bitcoin below 85,000 USD and shaving around 12% off Strategy’s share price at the intraday low.

5. Scenario Analysis: BTC Above 100k vs. Below 80k

The real question is not whether Strategy could ever sell BTC in theory, but under what market conditions it might feel compelled to do so in practice. The company itself has hinted at two reference levels.

5.1 Upside scenario: BTC recovers above 100,000 USD

If Bitcoin climbs back above six figures and holds there, the impact on mNAV is straightforward. The value of Strategy’s BTC stack rises, its balance sheet strengthens and the stock is more likely to trade at a premium to net asset value. In such an environment:

- Raising additional equity becomes easier and potentially accretive.

- Existing debt looks more manageable relative to asset value.

- The probability of needing to sell BTC to fund dividends or obligations diminishes.

In this upside path, the company can continue its long-standing playbook: issue shares opportunistically, use proceeds to buy more Bitcoin, and position itself as a long-term accumulator. For investors, the main discussion would then focus on how much leverage is prudent and whether the equity premium over NAV is justified.

5.2 Stress scenario: BTC falls and stays below 80,000 USD

The more challenging environment is one where Bitcoin moves decisively lower and remains there for an extended period. Management has referenced 80,000 USD as a rough line where pressure could build, though the precise threshold depends on other factors such as interest rates, credit conditions and overall market sentiment.

If BTC were to trade well below that level while mNAV remained under 1x, several things could happen:

- The value of the BTC holdings would shrink, reducing the cushion behind the company’s debt.

- Equity raises would become more difficult, as the market might be unwilling to pay even the current implied value of the assets.

- Ratings agencies and lenders could become more cautious, increasing refinancing costs.

With 1.44 billion USD in reserve, Strategy would still have time to navigate such a period. It could adjust dividend policies, reduce discretionary spending, renegotiate terms or seek strategic investments. Only if these tools proved insufficient, and if the discount to mNAV persisted, would using a portion of the BTC stack become a realistic option.

Even then, a sale would not necessarily mean liquidating the entire treasury. The company could choose to sell a small portion to restore flexibility while still holding a large core position. But the psychological impact on the market could be disproportionate to the number of coins involved, because it would break a long-standing assumption about the permanence of Strategy’s holdings.

6. Would a Strategy Sale Cause a 'Domino Effect'?

Some commentators worry that if Strategy ever sold, it could trigger a chain reaction: other institutional holders might follow, derivatives traders might rush to adjust positions and retail sentiment could weaken. Others argue that this risk is overstated and label the current debate as fear-driven.

Both perspectives capture part of the truth.

• From a liquidity standpoint, Bitcoin trades billions of dollars every day across spot and derivatives venues. Even a sizeable sale by a single company, especially if executed over time or via over-the-counter channels, would be large but not necessarily overwhelming relative to global volume.

• From a narrative standpoint, the effect could be more pronounced. Strategy has become a symbol of corporate adoption. A decision to sell, even temporarily, might lead some investors to question whether other treasuries will remain as committed during downturns. That uncertainty can amplify price swings in the short run.

In practice, markets often absorb such events more quickly than feared. If BTC were sold into a deep pullback, long-term buyers who had been waiting on the sidelines might view it as an opportunity. Over a multi-year horizon, the more important question is whether Bitcoin continues to gain adoption across a wide variety of holders, not whether one company adjusts its position at the margin.

7. What Investors Can Learn From the Strategy Debate

Regardless of how this specific story unfolds, it offers several useful lessons for anyone following Bitcoin and corporate adoption.

1. Corporate holders have different constraints from individuals. A listed company must consider dividends, debt covenants, regulatory filings and shareholder expectations. Even if leadership believes in Bitcoin for decades, it cannot ignore short-term funding realities.

2. Leverage amplifies both upside and downside. Using debt and equity issuance to buy BTC accelerates gains when prices rise, but it also tightens the margin for error when prices fall. Ratio metrics like mNAV are tools to track that balance.

3. Clear communication matters. Moving from 'never sell' to 'we may sell as a last resort' may be a responsible clarification, but it also shows why overly absolute statements can be risky in a world where conditions change.

4. Diversification of narratives is healthy. Bitcoin’s long-term story should not rest on any single company, fund or individual personality. The more distributed the set of holders and use cases, the less any one decision can move the entire market.

5. Indicators like mNAV help, but they are not guarantees. Watching the relationship between a company’s market cap and its asset value can highlight stress, yet it does not mechanically dictate future moves. Management judgment still plays a central role.

8. Conclusion: Between Conviction and Flexibility

Strategy’s latest comments do not mean that its Bitcoin strategy has been abandoned. The company continues to hold a large BTC position, has built a cash reserve of roughly 1.44 billion USD and still speaks about Bitcoin as a multi-decade treasury asset. At the same time, the leadership has now articulated what many observers assumed all along: there is a point at which protecting shareholders, honouring dividend commitments and managing leverage could require tapping that BTC reserve.

For the Bitcoin market, the key takeaway is not that a sale is imminent, but that even the most committed institutional adopters operate within a framework of financial discipline. Understanding that framework—cash runway, debt structure, mNAV and regulatory disclosures—gives investors a much clearer lens than simply repeating slogans.

Whether BTC next moves toward 100,000 USD or spends time below 80,000 USD will heavily influence how this story evolves. But in either case, the broader trend of digital assets integrating into corporate balance sheets is unlikely to be reversed by the actions of a single firm. Strategy may remain a high-profile example, yet it is only one piece of a much larger puzzle.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, investment, legal or tax advice, and it should not be treated as a recommendation to buy, sell or hold any digital asset or security. Digital asset markets are volatile and carry risk, including the possibility of total loss. Always conduct your own research and consider consulting a qualified professional before making financial decisions.