BlackRock’s Bitcoin ETF Has Negative Returns but Massive Inflows: What the Numbers Really Say

The snapshot from Bloomberg tells a story that looks contradictory at first glance. On a table dominated by broad equity and bond funds, BlackRock’s spot Bitcoin ETF IBIT stands out for two reasons:

- It sits in the top six US ETFs by year-to-date inflows, attracting roughly 25 billion USD of new money.

- It is the only fund in that top group with a negative return for the year so far.

Most investors instinctively focus on the red figure in the performance column: IBIT shows a year-to-date loss while products like VOO, IVV or GLD deliver solid gains. Yet flows tell a different story. Instead of exiting, investors are still adding capital to IBIT in size. Even more striking, IBIT has pulled in more fresh money than the flagship gold ETF GLD, despite gold being up more than 60% over the same period.

How can a fund that is down on the year still be a magnet for capital? To answer that, we need to separate three layers of analysis: what ETF flows actually measure, how traditional investors think about Bitcoin inside their portfolios, and what the 2025 data suggests about the next phase of adoption.

1. Flows vs. Performance: Two Very Different Signals

ETF tables often compress many dimensions into a few columns: assets under management (AUM), year-to-date flows, and performance. It is tempting to read them in a simple way—good funds rise and attract money; weak funds fall and lose it. Reality is more nuanced.

Performance reflects how the underlying asset has moved over a chosen time window. For a single-asset ETF like IBIT, that is essentially the price path of Bitcoin.

Flows, by contrast, record the net amount of new capital that investors have added or withdrawn. A fund can have:

- Positive performance and negative flows, if investors are taking profits or reallocating to other assets.

- Negative performance and positive flows, if investors are buying into weakness or building positions for the long term.

IBIT clearly falls into the second category. The negative return tells us that, measured from 1 January to today, Bitcoin’s price is lower. The strong inflow tells us that many investors view that decline as an opportunity rather than a reason to leave. They are using the ETF structure to scale into positions over time, not simply to chase short-term momentum.

2. Who Is Buying IBIT, and Why?

The identities of every buyer are not public, but several patterns have emerged since US spot Bitcoin ETFs launched:

• Advisory platforms and wealth managers use IBIT and its peers to allocate small slices of client portfolios to Bitcoin without having to manage wallets, private keys or exchange relationships.

• Institutional investors such as family offices, hedge funds and some asset managers prefer listed products for operational, regulatory and reporting reasons. An ETF held in a brokerage account fits existing workflows.

• Self-directed retail investors who already trade equities and ETFs may find it simpler to add IBIT to an existing account than to open a separate crypto exchange account and manage direct holdings.

For all of these groups, IBIT is less a short-term trading vehicle and more a compliance-friendly access point to Bitcoin as an asset class. When they decide to build exposure, they often do so via planned allocations—say 1–3% of a diversified portfolio—rather than rapid in-and-out trades.

That behaviour helps explain why flows can remain positive even through a difficult year. Many investors are still in the “initial build-up” phase of their Bitcoin allocation. Price dips simply change the entry level at which scheduled purchases execute.

3. What Negative Returns with Strong Inflows Actually Mean

From an analytical perspective, the combination of a negative year-to-date return and very strong inflows carries several important messages.

3.1 Long-term conviction over short-term pain

If most IBIT investors were purely focused on this year’s number on their statement, a negative return would be a powerful deterrent. Instead, they keep allocating cash. That suggests they are working from a multi-year thesis about Bitcoin’s role—as a potential store of value, a hedge against currency debasement, or a high-volatility growth asset—rather than a single-year trade.

3.2 Dollar-cost averaging at scale

A negative return plus steady inflows is mechanically similar to classic dollar-cost averaging. When the price drops, each new contribution buys more units. For investors who believe in the long-term trajectory of the asset, this approach can reduce the average purchase price over time. In IBIT’s case, the table implies that billions of dollars are being deployed according to that philosophy, whether through explicit plans or implicit rebalancing mandates.

3.3 A rising base of committed capital

ETF flows also speak to market structure. Every unit of IBIT represents a corresponding amount of Bitcoin held by BlackRock’s custodians. Persistent inflows therefore mean that a larger and larger quantity of BTC is being absorbed into a vehicle typically held by slow-moving, regulation-sensitive investors. That can change the composition of the holder base in ways that are relevant for volatility and supply dynamics, even if it does not guarantee any specific price outcome.

4. Outpacing Gold: Why IBIT vs. GLD Matters

One of the most eye-catching details in the Bloomberg screenshot is that IBIT’s year-to-date inflow exceeds that of GLD, the long-standing flagship gold ETF. This is notable for several reasons:

- GLD is backed by a metal with thousands of years of monetary history and is widely used by institutions as a portfolio diversifier.

- In the period shown, gold has returned more than 60%, a very strong performance by historical standards.

- Despite that outperformance, net new money flowing into IBIT is larger.

The implication is not that gold is losing relevance overnight, but that Bitcoin is increasingly viewed as a strategic asset that deserves a seat next to gold rather than in a separate, purely speculative category. When a conservative institution chooses to allocate new capital, the marginal dollar is increasingly split between traditional safe-haven assets and digital ones.

For the crypto ecosystem, this shift is significant. It signals that the conversation has moved from “Should we ever touch this?” to “What is the right allocation size and the best vehicle?”

5. Reading the Table from a Portfolio-Construction Lens

Placing IBIT alongside broad equity funds like VOO and IVV, bond funds such as BND, and commodity products like GLD reveals how traditional allocators are thinking about Bitcoin in 2025.

- VOO, IVV, VTI and similar funds remain core building blocks. Their inflows reflect the continual funneling of retirement contributions and systematic investment plans into diversified baskets of stocks.

- GLD and other alternatives provide diversification against equity risk and currency uncertainty.

- IBIT now sits in the same flow league as these giants, even in a year when its price performance is negative. That suggests Bitcoin is being slotted into the same mental category: a strategic component of long-horizon portfolios.

From a risk-management standpoint, most institutions are unlikely to make Bitcoin a dominant allocation. Instead, they blend a small slice of IBIT exposure into a much larger mix of stocks, bonds and real assets. The table is consistent with that approach: huge absolute inflows, but still small relative weights compared with total assets in mainstream funds.

6. Why a “Bad” Year Can Build the Next Cycle’s Foundation

It is intuitive to think of a weak price year as purely negative. Yet in markets with long adoption curves, down periods often play a constructive role:

• They test conviction. Investors who continue to add capital during unfavourable price action are revealing that their thesis is not purely narrative-driven; it is rooted in a longer view of technology, monetary policy and network effects.

• They improve entry points for new participants. If an institution’s investment committee approved a Bitcoin allocation at much higher prices but moved slowly, price declines coupled with the availability of a familiar ETF wrapper can actually make it easier to justify implementation.

• They anchor long-term holders. Positions initiated in a difficult year may become part of the “strong hands” base, less likely to be liquidated on the first sign of volatility in future cycles.

IBIT’s 2025 profile fits this pattern closely. Even though the ETF shows a negative year-to-date return, the decision by investors to keep allocating sends a message: they perceive current prices as acceptable entry levels for a multi-year thesis, not as a signal to abandon the idea.

7. Educational Takeaways for Individual Investors

For readers who are not institutional allocators but are trying to understand what IBIT’s data means, there are several key lessons:

• Do not read flow tables in isolation. Strong inflows do not guarantee future gains, and negative returns do not automatically mean an asset is “broken.” Both metrics need to be viewed in the context of time horizon and investor type.

• Understand your own thesis before following large investors. Institutions may have different objectives, risk tolerance and constraints. The fact that they are comfortable adding IBIT does not mean the same allocation is appropriate for everyone.

• Consider diversification and position sizing. Many professional portfolios treat Bitcoin as a small but meaningful allocation rather than an all-or-nothing bet. Thinking in terms of percentages of overall wealth, rather than absolute amounts, can help frame risk more clearly.

• Remember that ETFs simplify access but not price risk. Buying IBIT avoids dealing with wallets and key management, but the underlying asset remains volatile. A convenient wrapper does not change that fundamental characteristic.

8. What to Watch Going Forward

If IBIT’s 2025 experience is a preview of future cycles, several indicators will be important to track:

• Whether flows stay positive through volatility. Sustained inflows across different market conditions would reinforce the interpretation that Bitcoin has become a structural allocation for many investors.

• How IBIT’s AUM behaves relative to price moves. If assets under management remain stable or grow even after large drawdowns, it would suggest that net new capital is offsetting mark-to-market losses.

• Comparisons with alternative stores of value. The ongoing race between IBIT and GLD inflows provides a real-time gauge of how investors balance traditional and digital hedges.

• Regulatory and product developments. The introduction of more ETF options, potential tax-advantaged wrappers or derivatives based on spot ETFs could further entrench Bitcoin’s place in mainstream portfolios.

9. Conclusion: A Year That Looks Bad on a Chart but Good in a Spreadsheet

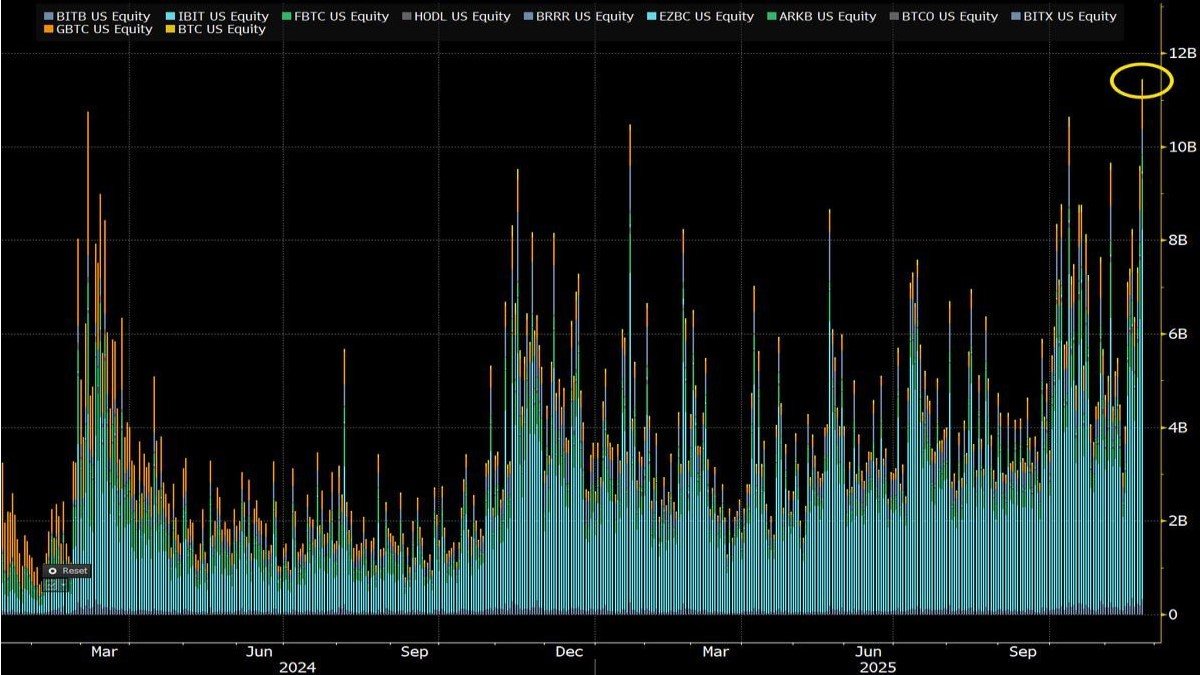

On a simple price chart, 2025 has not been kind to IBIT holders. The ETF’s year-to-date return is negative while many stock and gold funds show healthy gains. Yet the Bloomberg table highlights a different dimension: approximately 25 billion USD of net new money has flowed into the fund, placing it among the most popular ETFs in the United States.

For a young asset class still working to earn trust within traditional finance, that pattern may be more important than any single year’s percentage change. It means that a growing base of investors—many of them conservative by nature—are choosing to treat Bitcoin as a strategic allocation and are willing to endure volatility to pursue that thesis.

Whether those bets pay off in the coming years remains uncertain. But from the vantage point of market structure and adoption, IBIT’s combination of red performance numbers and green flow figures is a powerful signal: Bitcoin is no longer just a trade on the margins; it is gradually becoming part of the core toolkit for mainstream portfolios.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment, legal or tax advice. Digital assets and exchange-traded products can be volatile and may not be suitable for every investor. Always conduct your own research and consult a qualified professional before making financial decisions.