Tom Lee’s Bitmine Keeps Buying and Staking ETH: Why Corporate Ethereum Treasuries Are a Different Kind of Demand

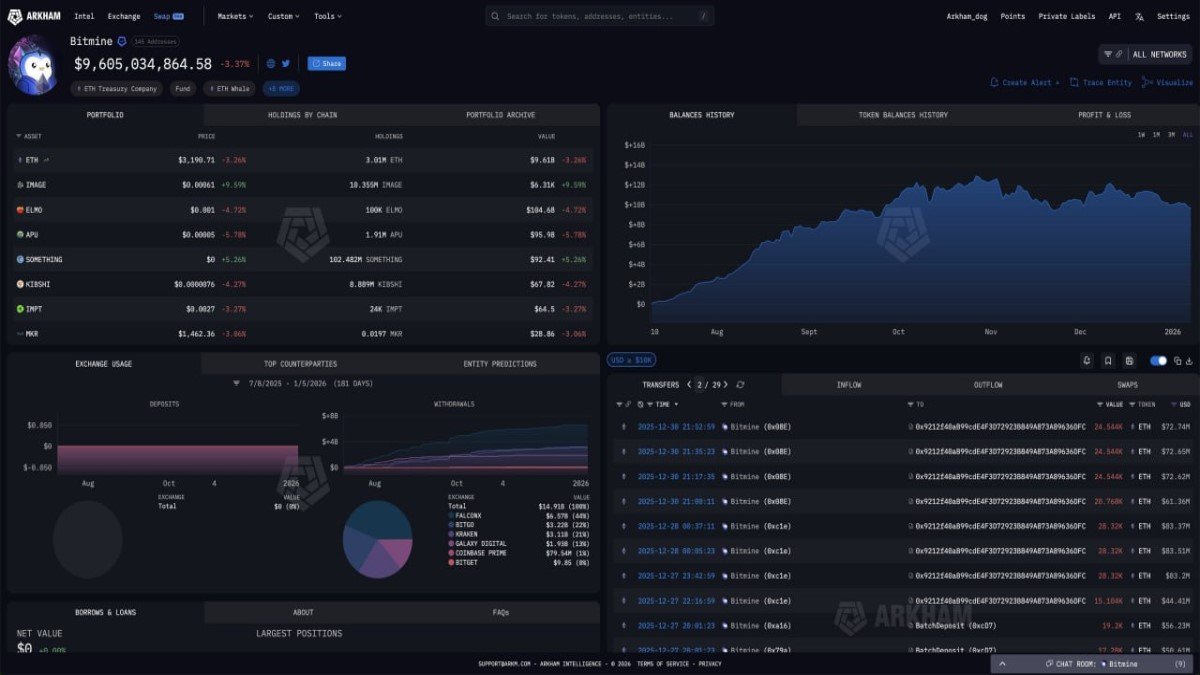

When people say “don’t care about short-term noise,” it’s usually a motivational quote pasted over a candle chart. But sometimes it’s an operating model. The story around Tom Lee’s Bitmine—reported as buying roughly $105.3M of ETH in the past week, lifting total holdings to about $13.23B, with around $1.46B staked and a headline claim of ~3.43% of ETH supply—reads less like a trade and more like a treasury blueprint.

That difference matters. A trader buys ETH and hopes other people buy later. A treasury buyer buys ETH and then asks a second question: “How do we make the ETH we hold work?” Staking is the answer—and it changes the character of demand. It’s not only a bet on price; it’s a bet on Ethereum as productive infrastructure.

From “Whale Buy” to “Balance-Sheet Flywheel”

Let’s start with the part everyone understands: a large buy can tighten spot supply and improve sentiment. But the more durable impact comes from what happens after the purchase. If a treasury buyer stakes, ETH transitions from liquid inventory into a yield-bearing position with constraints, timelines, and operational risk. That’s not a trivial switch—it’s a change in the market’s plumbing.

This is why the phrase “Tom Lee is still buying and staking” lands differently than “a whale bought ETH.” One is a recurring decision process; the other is a single print on a tape. Recurring processes create regimes. Regimes are what investors live through.

• A trader’s loop: buy → wait → sell (or get forced out).

• A treasury-staker’s loop: buy → stake → manage risk/withdrawals → repeat → communicate to stakeholders.

If that loop persists, it can form a “balance-sheet flywheel”: holdings grow, staking rewards accumulate, the entity’s financial narrative strengthens, and the ability to keep allocating becomes easier. That doesn’t guarantee price goes up—nothing does—but it shifts the market from episodic demand to programmatic demand.

Staking Turns ETH Into a “Native Rate,” and That Reprices Expectations

In traditional markets, investors obsess over yield curves because yield sets the “price of patience.” Ethereum staking introduces a native on-chain rate—imperfect, variable, and operationally complex, but conceptually powerful. It creates a baseline return that is not derived from lending to someone else; it is derived from participating in consensus.

For a corporate treasury, that’s attractive for a simple reason: it reframes ETH from “volatile asset” into “productive asset.” The moment a finance team can say “we earn yield for providing security,” the internal conversation changes. You’re no longer only defending exposure; you’re explaining a business-like function.

• Price thesis: ETH appreciates if demand for blockspace and economic activity grows.

• Productivity thesis: ETH can generate ongoing rewards (and potentially align with real on-chain usage).

The second thesis is what makes ETH treasuries structurally different from BTC treasuries. Bitcoin is optimized for scarcity and settlement; Ethereum is optimized for execution and coordination. Staking is the bridge between holding and participating.

Liquidity Isn’t Just “How Much ETH Exists”—It’s “How Much ETH Can Hit the Market Fast”

The headline numbers—$13.23B held, $1.46B staked—sound like a supply shock. But the mature way to think about this is not “supply removed forever.” Staked ETH is not destroyed; it is time-bounded liquidity. Unstaking takes time, and large exits can face queue dynamics. That delay changes how quickly selling pressure can materialize during stress.

So the real effect of staking at scale is a change in liquidity elasticity:

• In a fast drawdown, staked positions can’t instantly become sell pressure, which can dampen reflexive cascades.

• In a prolonged risk-off regime, staking doesn’t prevent selling—it just schedules it, potentially turning panic into a slower bleed.

This is why “not caring about short-term moves” is rational for a staker. The system itself forces the strategy to be longer-term. You can’t easily scalp a position that is operationally committed.

The Hidden Cost: Operational Risk Is the Price of Yield

Retail often treats staking like a savings account: click a button, collect yield. Corporate-scale staking is closer to running infrastructure. You introduce risks that spot holders don’t face, including validator performance, slashing events, counterparty exposure (if using providers), and governance/upgrade risk.

For a large treasury, the question becomes: “Are we being paid enough to accept these risks?” That answer depends on operational maturity. A disciplined institution can treat staking yield as a reward for competence. A sloppy institution can treat staking yield as a trap that converts financial risk into technical risk.

Three practical implications follow:

• Staking yield is not ‘free.’ It is compensation for reliability and the acceptance of protocol rules.

• The market may eventually price ‘staking quality.’ Not all yield is equal if the risk profile differs.

• Narratives can flip quickly. If anything goes wrong operationally, a “smart treasury” story can become a “why was this risk taken?” story.

Concentration: When “Bullish” Looks Like a Governance Problem

Claims like “holding ~3.43% of total ETH supply” (as stated in your prompt) are psychologically loud. Even if the exact share varies over time, the direction is clear: accumulation at that scale invites a different debate—less about price, more about concentration.

Ethereum’s strength is credible neutrality: no single party should be able to dictate outcomes. Large holders don’t automatically control the network, but staking concentration can influence the validator landscape, social consensus discussions, and perceptions of decentralization—especially among regulators and institutions that care about governance optics.

The paradox is this:

• Big treasuries can validate Ethereum’s legitimacy (institutions participate, capital commits, infrastructure professionalizes).

• Big treasuries can also raise discomfort (too much influence, too few hands, “is this still credibly neutral?”).

That tension is not bearish or bullish by default. It’s a structural tradeoff the ecosystem must manage as it grows up.

What This Signals About 2026: ETH Demand Is Getting “Accounting-Aware”

One of the least discussed shifts in crypto is how the buyer profile is changing. Early cycles were dominated by discretionary flows: traders, retail waves, and momentum funds. The newer wave includes entities that must explain themselves to auditors, boards, and risk committees.

That changes behavior in two ways:

• Positioning becomes stickier. These players don’t flip on a headline; they operate on policy and mandate.

• Selling becomes more procedural. Exits are risk-managed, staged, and often telegraphed indirectly through public filings or operational changes.

So when you see a treasury buyer continue to buy and stake into noise, the takeaway isn’t “price must go up.” The takeaway is: ETH is increasingly being treated as an asset that fits an institutional operating model. That can reduce the frequency of panic cycles—but it can also create new kinds of shocks if policy changes or compliance constraints suddenly tighten.

How to Read On-Chain Treasury Activity Without Falling Into the “Buy = Moon” Trap

It’s tempting to use dashboards as a scoreboard: deposits mean selling, withdrawals mean buying, staking means bullish. Reality is messier. Treasury activity often includes internal rebalancing, custody moves, and operational restructuring that look dramatic on-chain but are neutral in intent.

A more durable framework is to ask three questions:

• Intent: Is this entity running a long-duration strategy (stake, hold) or trading inventory?

• Constraints: How quickly can they change their mind (unstake timelines, custody policies, board approvals)?

• Incentives: What do they gain by holding—price upside only, or price + yield + strategic positioning?

In the Bitmine narrative, the incentives appear aligned with a long-duration stance: keep buying, keep staking, ignore short-term wobble. That’s not a promise of higher prices. It’s a signal that at least some large players are building for a world where Ethereum is not a trade—it’s a balance-sheet allocation with a productivity component.

Conclusion: The Most Bullish Part Isn’t the $105M Buy—It’s the Repetition

Markets don’t transform because one whale bought once. Markets transform when behavior becomes repeatable. A reported $105.3M ETH purchase is impressive; a pattern of buying and staking is more important. It suggests a shift from speculative demand to policy-driven demand—and that’s how asset classes mature.

The catch is that maturity is not a one-way street. Treasury staking introduces new risks: operational complexity, concentration optics, and the possibility that institutions act in correlated ways when rules change. The opportunity is equally real: if Ethereum is increasingly held by actors who can afford patience and who earn yield by securing the network, the market’s downside dynamics can look different from older cycles.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Nothing herein is a recommendation to buy, sell, or hold any asset. Digital assets are volatile and carry risk, including the risk of total loss.

Frequently Asked Questions

Does large-scale staking guarantee ETH price will rise?

No. Staking can change liquidity and investor behavior, but price still depends on broader adoption, risk sentiment, and macro liquidity. Staking can dampen some panic dynamics, yet it can’t eliminate drawdowns.

Is staked ETH “removed from supply”?

Not permanently. Staked ETH is locked into an operational process. It can be withdrawn, but typically with timing constraints. The key effect is time-bounded liquidity, not total removal.

Why do corporate treasuries staking ETH matter more than normal whales?

Because corporate strategies tend to be programmatic and policy-driven. That can make demand stickier, but also creates correlated behavior if regulations, accounting rules, or internal mandates change.

What’s the biggest risk of staking at scale?

Operational risk and concentration optics. Staking yield comes with validator performance requirements, protocol rules (including slashing), and reputational/regulatory scrutiny if staking power concentrates in too few hands.

How should readers interpret on-chain dashboards like Arkham?

As context, not as a verdict. Wallet movements can reflect custody changes, internal treasury ops, or risk controls. The best interpretation focuses on intent, constraints, and incentives—not a single transfer.