Ethereum’s Upgrade Cycle: Why Every Hard Fork Feels Like a Value Jump

In day-to-day trading, Ethereum often gets reduced to a ticker on a screen: a percentage change over the last 24 hours, a funding rate, a chart pattern. But under the surface, the last few years have been defined by something deeper and slower-moving: an upgrade cycle that keeps changing what Ether actually is as an asset. Each major milestone has either reduced structural supply or expanded the usefulness of the network. That is the kind of shift that rarely shows up in a single session, but it matters far more than any 24 hour candle.

To understand why professional investors increasingly talk about Ether in the same breath as yield curves, fee markets and balance sheet management, you have to zoom out from price and look at the protocol itself. Since 2021, Ethereum has gone from a proof of work chain with a fairly standard inflation schedule to a proof of stake settlement layer that can be net deflationary at times, while powering a growing web of layer 2 networks on top. It is not just another inflationary coin any more; it behaves more like a piece of economic infrastructure for the wider digital asset ecosystem.

From “Inflation Coin” Meme to Structural Scarcity

For years, one of the most common critiques of Ether from Bitcoin-focused investors was simple: the supply was not capped. Bitcoin had a hard-coded limit and halving schedule, while Ether did not, so the argument went that it would always be an inflationary asset that could be diluted indefinitely.

That view already started to age when Ethereum introduced a new fee model via EIP-1559, which began burning a portion of transaction fees. Once the network became busy, that burn offset a meaningful share of new issuance. The real break with the past came with the move from proof of work to proof of stake in the Merge. Under proof of work, the chain had to issue a large amount of new Ether every day to pay miners for hardware and electricity. Under proof of stake, the security budget is mostly denominated in opportunity cost and smart contract risk rather than power plants, so the required issuance is materially lower.

If you step back and look at the combination of lower issuance and ongoing fee burns, Ether now has a supply profile that can swing between modestly inflationary and modestly deflationary depending on network usage. It is not a hard cap like Bitcoin, but it is also nowhere near the perpetual inflation model that the old meme suggests. In other words, Ether’s monetary policy has become a function of the network itself: the more it is used, the more likely it is that net supply shrinks over time.

The Upgrade Cycle as a Value Engine

What makes Ethereum unusual is not just that it upgrades, but that its upgrades keep changing the economic properties of the network in ways that are directly relevant to holders. Three recent milestones illustrate the pattern.

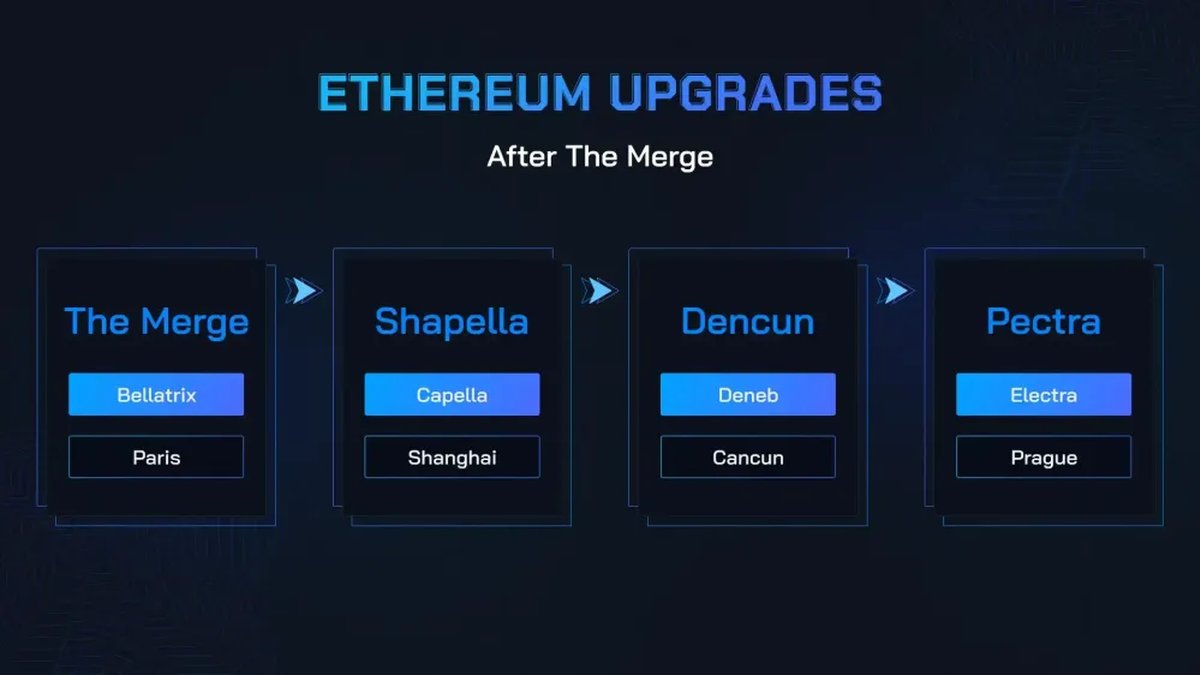

The Merge: Energy, Issuance and Credibility

The Merge replaced proof of work with proof of stake. From a pure branding perspective, the headline was about energy: drastically lower power consumption and a smaller environmental footprint. For institutional allocators bound by ESG or sustainability mandates, that was not a cosmetic detail. It took a large objection off the table and made it easier to justify Ether exposure inside traditional portfolios.

Under the hood, however, the Merge was also a change to the supply engine. With miners retired, the network no longer had to subsidise industrial-scale hardware and energy bills. Issuance dropped sharply, turning what used to be a structurally inflationary asset into something much closer to a self-adjusting commodity, where usage and security requirements determine how much new Ether actually has to be created.

Shanghai: Unlocking Staked Ether and Maturing the Yield Curve

The Shanghai and Capella upgrades, often referred to together as Shanghai, enabled withdrawals for staked Ether. Before that, staking rewards existed on paper, but not as a fully liquid part of the asset’s lifecycle. Investors could deposit and earn, but they had no guaranteed path to exit via the protocol itself.

After Shanghai, Ether staking started to look less like a one way speculative position and more like a yield curve. Stakers gained the ability to enter and exit, restake or rotate across providers, and price the risk of doing so with more confidence. That helped large, regulated players who need clear exit mechanics and operational playbooks. It also anchored a new way of thinking about Ether: not just as a volatile asset, but as a security primitive that can generate cash-like flows when locked into the consensus layer.

Dencun: Scaling Data, Not Just Block Space

The Dencun upgrade shifted the focus to data availability and layer 2 economics. By introducing a new transaction type for cheaper data storage, it gave rollups a lower cost base for publishing their compressed transaction data back to mainnet. In plain language, Dencun made it cheaper for layer 2 networks to exist on Ethereum without constantly running into fee ceilings.

That sounds technical, but the implications are simple. If layer 2 networks can settle more activity onto Ethereum at lower cost, they can support more users, more applications and more complex markets without congesting the base chain. Over time, that means more total transactions flowing through the Ethereum stack, more fees to be burned and more reasons for developers to keep building on this particular settlement layer rather than elsewhere.

Seen together, these upgrades form a consistent pattern. Each one either reduces the net supply of Ether required to keep the chain secure or increases the volume and quality of economic activity that can run on top of it. In traditional finance, that combination of harder supply and growing demand is exactly what makes an asset interesting to long term investors.

Bitcoin as Digital Gold, Ether as Digital Energy

Comparisons between Bitcoin and Ethereum often devolve into zero sum arguments about which one is superior. A more useful framing is to treat them as complementary pieces of financial infrastructure that play different roles.

Bitcoin behaves like a form of digital gold. It is simple by design, with a fixed supply schedule and a narrow set of consensus rules that change very rarely. Its primary job is to be a durable store of value and a censorship resistant asset that does not depend on any one institution. Investors who want something that looks and feels like a non sovereign reserve asset tend to gravitate toward that simplicity.

Ether, by contrast, looks more like the energy that powers a digital economy. It is the asset you need to pay for computation, to settle transactions across a web of smart contracts and layer 2 networks, and to secure the chain via staking. Fees are like electricity prices, and upgrades are like improvements to the grid. When the network becomes more efficient, the cost of running applications can fall even as total throughput rises. When activity increases, more fee revenue is generated and more Ether is burned.

In that analogy, Ether is not trying to compete with Bitcoin as a mirror image of digital gold. It is occupying a different spot in the stack: the resource that fuels programmable money, tokenised assets and on chain coordination. The fact that it has become structurally scarcer over time is a by product of making that energy system more efficient, not an attempt to mimic a hard capped monetary policy.

What the Last 24 Hours Tell You – and What They Do Not

Over any given 24 hour window, Ethereum’s market behaviour can look noisy. Headlines may highlight funding flips, liquidations on highly leveraged positions, or short term rotations between Ether and newer narratives. Those details matter for traders who manage intraday risk, but they do not change the underlying direction of travel for the network itself.

When you look at the most recent session through the lens of the upgrade cycle, three themes stand out:

- Staking participation keeps trending higher, which means a growing share of Ether behaves like infrastructure capital rather than free floating speculative supply.

- Layer 2 networks continue to compete on fees and user experience, but they converge on Ethereum as the settlement layer, reinforcing the role of mainnet as a neutral hub.

- Fee markets oscillate with activity, yet the burn mechanism remains in place, quietly counteracting issuance whenever utilisation picks up.

None of these shifts are dramatic enough to dominate a daily chart, but they compound. A marginally lower free float, a marginally more efficient scaling stack and a marginally stronger perception of Ethereum as credible infrastructure all add up over time. In that sense, the most important market story for Ether is not whether it outperformed or underperformed in the last 24 hours, but whether the upgrade engine is still running as designed.

Risks, Trade offs and Open Questions

A brand safe analysis also has to acknowledge what could go wrong. Ethereum’s upgrade cycle, while impressive, is not without risk. Each change to the protocol introduces new complexity. The more moving parts there are, the more work clients, validators and developers have to do to keep the system synchronised and secure.

On the economic side, a net deflationary asset is attractive on paper, but it can also create tensions. If fee levels remain high for extended periods, usage may migrate to other chains. If they remain too low, the burn may not be strong enough to offset issuance, and the scarcity narrative may weaken. The protocol is effectively trying to balance user affordability, validator incentives and holder expectations at the same time.

There are also external uncertainties. Regulators are still refining their views on staking, yield bearing tokens and the line between infrastructure and investment product. Competing layer 1 chains continue to innovate, sometimes by prioritising simplicity and throughput over the kind of modular, rollup centric design that Ethereum favours. And macro conditions still shape how much risk investors want to take in any volatile asset, regardless of how elegant its monetary policy has become.

How Long Term Investors Can Read the Upgrade Cycle

For long horizon participants, the key is to separate structural signals from short term noise. In practical terms, that means paying more attention to variables like staking participation, layer 2 transaction volumes, fee burn trends and successful execution of roadmap milestones, and less attention to intraday headlines about liquidation spikes or social media sentiment.

If Ethereum continues to move along its current path, each upgrade should either make the network more useful, more secure or more economically efficient. That does not guarantee any particular price outcome, and it does not mean Ether will behave like a low volatility bond. But it does mean the asset is increasingly backed by something tangible: a live, evolving piece of digital infrastructure that other systems rely on.

Bitcoin can keep playing its role as digital gold: a simple, robust store of value anchored by a fixed supply schedule. Ether can keep evolving as the energy layer of the digital economy: a flexible, programmable resource whose scarcity emerges from usage and design rather than from a single hard cap number. Investors do not have to choose a winner between those roles; they simply have to understand what each asset is actually doing under the hood.

This article is for informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Digital assets are volatile and may not be suitable for all investors. Always conduct your own research and consider speaking with a qualified professional before making financial decisions.