Bitcoin as a $1.2T Fiat Magnet: The Gateway Effect Behind Crypto’s Capital Funnel

Crypto markets love new narratives, but capital is more conservative than storytelling. When investors show up with fresh fiat, they tend to buy what feels most legible first—an asset whose “mental model” fits inside existing financial instincts. That’s why the most interesting part of the latest fiat-purchase snapshot isn’t the ranking itself. It’s the pattern: capital doesn’t enter crypto evenly. It pours through a narrow funnel, then spreads outward.

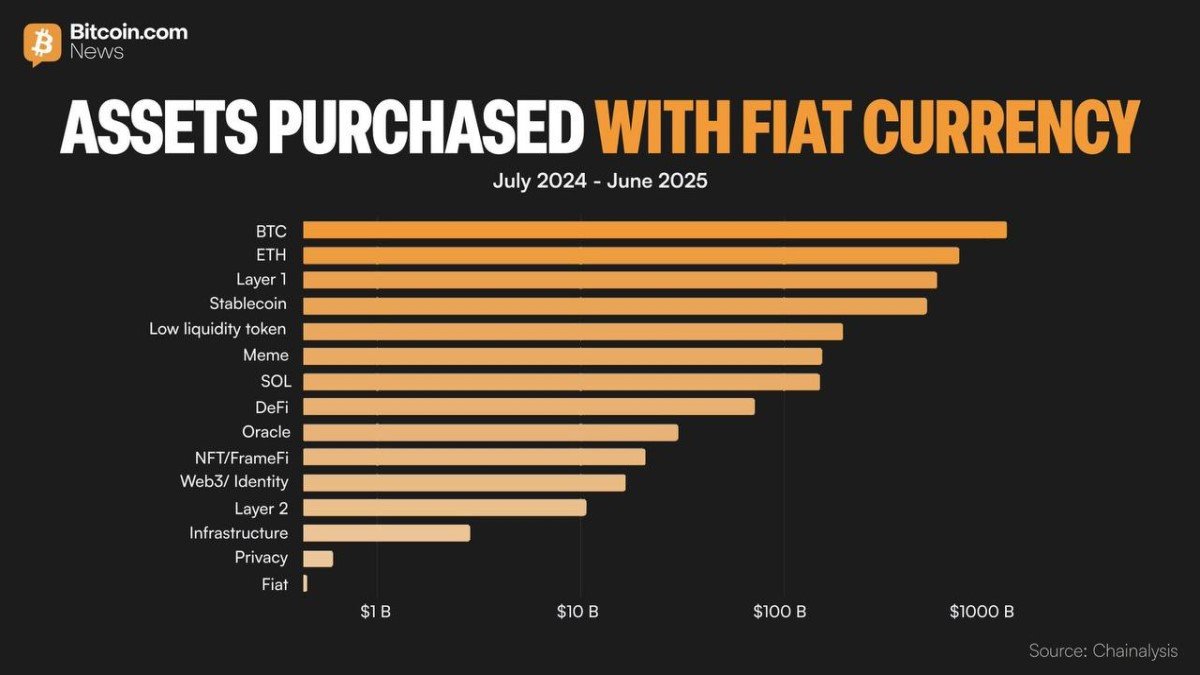

In a chart summarizing assets purchased with fiat currency from July 2024 to June 2025 (attributed to Chainalysis in the graphic), Bitcoin leads at roughly $1.2T, followed by Ethereum at about $724B, other Layer 1s around $564B, and stablecoins near $497B. These figures should be treated as directional, but the hierarchy is hard to miss: BTC is the first stop for new money more often than anything else.

1) What the chart is really measuring (and what it isn’t)

The phrase “purchased with fiat” sounds straightforward, but it’s worth slowing down. This metric is best read as: when money enters from traditional currency rails into the crypto ecosystem, what does it buy first? It’s not the same as market cap growth, and it’s not the same as “net new demand” after accounting for churn, transfers, or internal rotations.

In other words, this isn’t a scoreboard for “best asset.” It’s a map of the on-ramp. And on-ramps reveal something fundamental: the asset that dominates fiat entry tends to become the market’s reference point—pricing anchor, liquidity anchor, and often the psychological anchor for risk appetite.

2) Why Bitcoin attracts the first wave of fiat

If you zoom out, Bitcoin is not winning because it has the most features. It’s winning because it has the simplest story that can survive contact with institutional process. When compliance teams, investment committees, and custody providers evaluate crypto exposure, they don’t begin with “what’s exciting.” They begin with “what’s defensible.”

Bitcoin’s defensibility comes from a bundle of attributes that look familiar to traditional allocators: a long operating history relative to the asset class, deep liquidity, broad market infrastructure, and a narrative that resembles a reserve asset more than a startup. Even investors who don’t fully embrace the philosophy can understand the structure: scarcity, global tradability, and no single issuer controlling supply.

That combination produces what I call the gateway effect: BTC becomes the asset people buy before they decide whether they are “crypto people.” It’s the waiting room where new capital sits while it learns the building’s layout.

3) The capital stack: reserve, application layer, venture beta, and settlement

The most useful way to interpret the ranking is not as a beauty contest, but as a capital stack—a set of roles that different crypto assets play in a portfolio and in the broader system. The chart’s top categories line up cleanly with four roles.

• Bitcoin (Reserve Role): Often treated as the primary store-of-value narrative inside crypto, and the most common “first allocation.”

• Ethereum (Application Infrastructure Role): Often associated with the onchain economy—smart contracts, tokenized assets, and the base layer for composable finance and apps.

• Other Layer 1s (Venture Beta Role): Typically reflect higher growth expectations and higher dispersion of outcomes. They attract capital that is explicitly seeking upside through ecosystem expansion.

• Stablecoins (Settlement Role): Frequently used as the system’s working capital—dry powder, payment rail, and accounting unit inside exchanges and onchain markets.

This is why BTC being #1 doesn’t “kill” the rest of crypto. It often funds the rest of crypto. The gateway effect creates a sequence: fiat enters → BTC absorbs trust → risk appetite grows → capital fans out into infrastructure, apps, and higher beta segments.

4) Why Ethereum remains second: utility that can be priced

Ethereum’s position near the top is a reminder that utility matters—but it must be utility that markets can translate into a valuation framework. Ethereum’s strongest narrative isn’t “it’s faster than everything.” It’s “it’s where activity aggregates when people want composability and deep developer tooling.” That makes ETH a proxy for onchain economic throughput, not just a token.

What’s subtle here is that Ethereum tends to capture demand in two forms at once: speculative demand (like most crypto assets) and infrastructural demand (because it powers a broad set of applications and settlement behaviors). When traditional capital grows comfortable, it often prefers the assets with multiple demand sources, not just one.

5) Other Layer 1s: the narrative of growth, and the price of competition

The “Layer 1” category after ETH represents something like a venture basket: capital seeking ecosystems that can compound adoption faster than incumbents. This is where crypto behaves most like early-stage tech investing—except the liquidity is higher and the sentiment cycles are faster.

But the same factor that attracts capital here—growth optionality—also creates fragility. L1 competition is brutal because switching costs can be low for certain user segments, while developer and liquidity incentives can shift quickly. The market is effectively pricing a contest: which networks will become durable venues for apps, trading, and settlement, and which will remain cycle-dependent?

6) Stablecoins: not the “fourth place,” but the hidden core

At first glance, stablecoins sitting below BTC and ETH might look like a secondary destination. In practice, stablecoins are often the least understood and most important category in the entire chart. They are the closest thing crypto has to a functional monetary layer: a unit that traders, businesses, and protocols use to quote prices, park value, and settle obligations.

Here’s the paradox: stablecoins can be central without being “exciting.” People don’t typically boast about holding stablecoins the way they talk about holding BTC. But stablecoins are where the system’s liquidity breathes. When markets get nervous, capital often rotates into stablecoins. When markets get active, stablecoins are what deploy into risk. In both cases, stablecoins are the bloodstream, not the spotlight.

7) Bitcoin as the onboarding asset: trust, simplicity, and institutional ergonomics

Why does the funnel start with Bitcoin instead of stablecoins, if stablecoins are so useful? Because stablecoins feel like “infrastructure,” and infrastructure requires trust in issuers, redemption processes, and regulatory frameworks. Bitcoin, by contrast, feels like “property” to many allocators—an asset you can custody and hold without needing to model an issuer’s balance sheet.

So BTC becomes the path of least resistance for first-time exposure. After that, stablecoins become the tool of least friction for operating inside the ecosystem. That division of labor is crucial: BTC is the entry narrative, stablecoins are the operating system.

8) Will stablecoins become a major ‘destination’ in 2026 and beyond?

Some observers expect stablecoins to become an even larger destination for fiat flows over time. That’s plausible, but the reason is not “people will prefer stablecoins over Bitcoin” in some simplistic rotation. The more realistic reason is that stablecoins can grow without users thinking they’re adopting crypto.

If stablecoins expand into cross-border settlement, business treasury operations, merchant tools, and back-office processes, then a larger share of fiat inflow will be directed into stablecoin rails first—because the user’s goal isn’t price exposure. The goal is movement: faster settlement, lower friction, broader access. In that world, stablecoins are not a speculative asset choice. They are a financial utility choice.

Still, this evolution comes with constraints that deserve attention: regulatory clarity, redemption reliability, banking partnerships, and transparency standards. Stablecoin growth is not only a tech story—it is a compliance and operational trust story.

9) What this funnel means for the next phase of crypto markets

When Bitcoin is the dominant fiat magnet, the entire market inherits a Bitcoin-shaped rhythm. Liquidity, sentiment, and risk tolerance often begin with BTC and then echo outward. That can make the market feel “monocultural” during stress, because correlations rise when the gateway asset is volatile.

But the same funnel structure also hints at maturation. Mature markets often have a dominant benchmark (BTC), a primary productive substrate (ETH), a competitive growth layer (other L1s), and a transactional monetary layer (stablecoins). That doesn’t remove volatility, but it does create a more legible architecture—one that traditional capital can understand, model, and integrate over time.

Conclusion

The headline “Bitcoin absorbed ~$1.2T of fiat-funded purchases” is impressive, but the deeper insight is structural: Bitcoin is functioning as crypto’s default gateway asset. It’s where new money goes to become comfortable. Ethereum captures the economy that runs on top. Other L1s absorb growth speculation. Stablecoins quietly power the day-to-day mechanics of liquidity and settlement.

If you want a single takeaway that feels different from typical news coverage, it’s this: crypto is not just a list of tokens competing for attention. It’s a capital funnel that channels trust first, then channels risk, and finally channels utility. Understanding that funnel is a form of risk management—because it explains why certain assets lead, why rotations happen, and why “adoption” can rise even when the loudest narratives temporarily fade.

Frequently Asked Questions

Does Bitcoin leading fiat inflows mean investors only care about BTC?

Not necessarily. It often means BTC is the first allocation—a gateway step. After onboarding, capital can diversify into other segments depending on risk appetite and the user’s goals.

Why are stablecoins so important if they rank below BTC and ETH?

Because stablecoins function as liquidity infrastructure. They are heavily used for settlement, collateral, and cross-platform movement, even when users are not seeking price exposure.

Should we treat these numbers as exact totals?

No. Treat them as directional indicators of where fiat-funded buying pressure concentrates. Different datasets and methodologies can produce different absolute values, but the funnel-like hierarchy is the main signal.

What would make stablecoins a bigger ‘destination’ for fiat flows?

If stablecoins expand further into payments, cross-border settlement, and business operations, more fiat inflows may target stablecoin rails first—because the motive becomes utility, not speculation.

Disclaimer: This article is for educational purposes only and does not constitute financial, investment, legal, or tax advice. Data points referenced from third-party visuals may be incomplete or methodology-dependent. Crypto assets are volatile and involve risk, including liquidity, regulatory, and operational risks. Always verify information using multiple credible sources and consider your own risk tolerance.