UNIfication: How Uniswap’s New Fee and Burn Model Rewires UNI’s Value Proposition

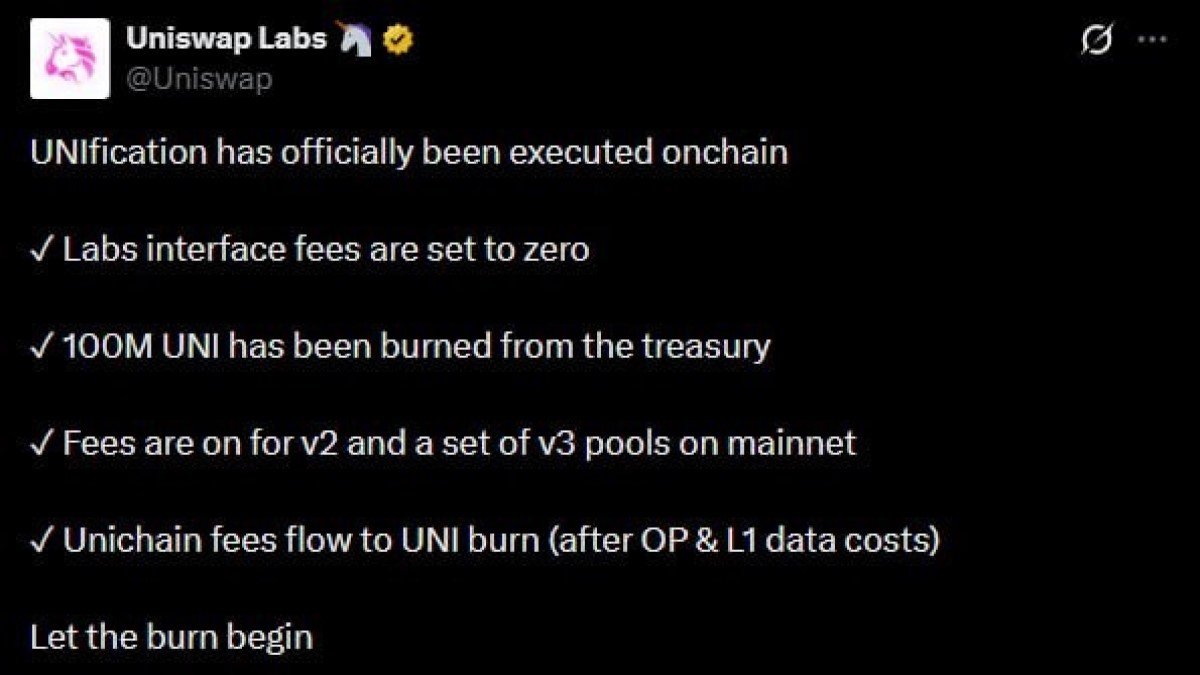

Very few governance proposals in decentralized finance attract as much attention as Uniswap’s UNIfication package. After years of debate about the so-called fee switch, the community has finally approved a bundle of changes that meaningfully alters how value flows through the Uniswap ecosystem. Protocol fees are now live on key pools, 100 million UNI have been removed from the treasury and permanently retired, front-end fees from Uniswap Labs have been reduced to zero, and an explicit framework has been created for routing future revenue through on-chain governance.

On the surface, this may look like a technical adjustment to a fee schedule. In reality, UNIfication tackles a long-standing question that has surrounded Uniswap ever since the UNI token was launched: is UNI only a governance token, or does it also have a direct and transparent relationship with the economic activity of the protocol? The answer after UNIfication is much clearer than before.

1. From Fee Switch Debates to a Coherent Value Strategy

When UNI was introduced in 2020, the design already mentioned the possibility of turning on protocol fees at some point in the future. In theory, a slice of the trading fees collected on Uniswap pools could be directed to the protocol treasury, rather than all of it flowing to liquidity providers. For several years, however, this mechanism remained dormant. At the same time, Uniswap Labs – the company that builds the reference front end – introduced a 0.25% interface fee on certain pairs, collected directly at the company layer.

This created a structural tension. The protocol remained free of fees at the governance level, while a private entity in the ecosystem collected meaningful revenue from the user interface. Holders of UNI saw large trading volumes and a dominant market share, yet the token itself had no direct link to the cash flows generated by the platform. It was difficult to argue that UNI captured the value of the protocol in a way that resembled traditional equity or even more modern digital assets with revenue sharing or buyback mechanisms.

UNIfication is designed to resolve this tension. Instead of relying on a company-centric model in which Uniswap Labs is the primary beneficiary of the protocol’s success, the new approach moves economic gravity back toward the protocol and its community. Labs can still build products and businesses around Uniswap, but the core mechanism for value capture now resides within the protocol itself and is controlled through governance.

2. The Five Pillars of the UNIfication Proposal

To understand the implications of UNIfication, it is helpful to separate it into five main components. Together, these elements form a new economic architecture for UNI.

2.1 Activating Protocol Fees on Key Pools

The first and most fundamental change is the activation of protocol fees on selected Uniswap v2 pools and on a set of v3 pools on Ethereum mainnet. Until now, almost all swap fees were directed solely to liquidity providers. Under the new model, a defined portion of those fees is diverted to the protocol as revenue. The exact percentage can be tuned by governance over time, but the core point is that Uniswap as a protocol now generates its own stream of income that does not depend on any private interface provider.

This revenue does not get paid out directly to token holders as a distribution. Instead, it is routed into a mechanism that removes UNI from circulation. In other words, protocol revenue is turned into token scarcity rather than immediate cash flow.

2.2 Burning 100 Million UNI from the Treasury

The second pillar is symbolic and mechanical at the same time: 100 million UNI have been transferred from the protocol treasury to a burn address, where they can never be moved again. At the time of the decision, this represented roughly 592 million USD worth of tokens. By retiring this allocation permanently, the community has reduced future circulating supply and sent a clear signal that long-term alignment is more important than maximizing discretionary budgets.

For years, observers worried that large treasury balances were a type of overhang. If those tokens were ever distributed carelessly or sold to fund short-term initiatives, they could put downward pressure on price and dilute existing holders. Burning a significant slice of the treasury reverses that narrative: instead of being viewed as potential sell pressure, the treasury is now smaller, and its remaining balance can be managed more prudently.

2.3 Setting Uniswap Labs’ Interface Fees to Zero

The third component addresses the role of Uniswap Labs. With UNIfication, the 0.25% interface fee that had been applied on the main Uniswap front end has been set back to zero. People who trade through the official app no longer pay that extra layer of cost. That decision has two important consequences.

First, the user experience is improved. In a competitive DeFi environment, fee levels matter, especially for smaller trades or high-frequency users. Removing the interface fee makes Uniswap more appealing relative to alternative trading venues and front ends.

Second, the move demonstrates that Labs is willing to prioritize the long-term health of the ecosystem over short-term revenue maximization. Instead of competing with the protocol for fee income, Labs is effectively stepping aside so that value can accumulate through the on-chain fee and burn mechanism that benefits the broader community.

2.4 Directing Unichain Sequencer Fees into UNI Burns

The fourth pillar looks beyond Ethereum mainnet. Unichain, a scaling solution closely integrated with Uniswap, collects sequencer fees from transactions that pass through it. Under UNIfication, net sequencer revenue from Unichain – after paying for L1 data and obligations to the underlying stack, currently OP – is also slated to flow into the UNI burn mechanism.

This effectively ties the success of Unichain to the token economics of UNI. As activity on Unichain grows, more fees are converted into UNI that is removed from supply. Instead of Unichain being a separate side business, it becomes part of a unified value loop that links user adoption, transaction throughput and token scarcity.

2.5 A Framework for Future Revenue Streams

The fifth and final element of UNIfication is forward-looking. The proposal sets a principle that future sources of protocol revenue – such as additional L2 deployments, Uniswap v4 features, UniswapX, protocol fee discount auctions or new aggregator hooks – will only be activated through explicit governance proposals. Each new revenue stream will have to specify how much is retained for operational needs, how much is burned, and whether any portion is used for other purposes such as ecosystem grants.

This framework gives the community ongoing control over the value flows that shape UNI. Instead of a one-time switch that is permanently locked in, UNIfication establishes a process: revenue opportunities are considered one by one, debated and configured in a way that preserves the core principle that the protocol, not only any single company, should be the primary beneficiary of its own success.

3. Economic Impact: From Pure Governance Token to Revenue-Linked Asset

Economically, UNIfication moves UNI closer to the category of assets whose value is influenced by protocol performance. The token is still a governance instrument, but its supply dynamics are now explicitly tied to on-chain revenues. The closest analogy in traditional finance would be a company that regularly uses a portion of its earnings to repurchase shares and retire them, instead of paying direct cash dividends.

3.1 Burning as a Form of Passive Buyback

Whenever protocol or sequencer fees are allocated to burning UNI, the effect is similar to an ongoing buyback program. Revenue generated by trading activity and network usage is used to remove tokens from circulation. Over long periods, if volumes remain strong or increase, this can meaningfully reduce the effective supply available on the market.

For analysts, this introduces a new line of inquiry. It is no longer sufficient to look at Uniswap’s total value locked or daily active users. One also needs to estimate how much annual revenue the protocol will generate, what fraction of that revenue is routed into burns, and how that compares with the existing circulating supply of UNI. Those parameters feed directly into models that try to estimate the token’s long-term value range.

3.2 Balancing the Interests of Traders, Liquidity Providers and Token Holders

Of course, every fee charged by the protocol must ultimately come from somewhere. If the protocol takes a share of swap fees, then either liquidity providers receive slightly less than before or traders pay a bit more in total costs. UNIfication attempts to strike a balance: the aim is to keep Uniswap’s pools competitive on pricing while still carving out a modest share of revenue for the protocol.

If the approach works, liquidity providers may benefit indirectly. A stronger UNI, anchored by predictable token economics and a transparent burn schedule, can attract more attention to the ecosystem, increase network effects and draw in additional order flow. That, in turn, may offset the small reduction in fee share through higher volumes and deeper liquidity.

4. Governance Consequences: More Power and More Responsibility for the DAO

UNIfication is not just about economics; it also redefines how the Uniswap DAO relates to the protocol. For the first time, governance has clear authority over tangible revenue streams and over the policies that determine how those revenues are used. That is both an opportunity and a challenge.

4.1 From Company-Centric to Protocol-Centric Value Capture

In the early years, many observers assumed that Uniswap Labs would remain the primary coordinator of development, infrastructure and ecosystem growth, while the DAO acted mainly as an advisory body. With UNIfication, the center of gravity shifts. The protocol itself collects revenue, and governance decides how aggressive the burn schedule should be and whether any funds should be redirected to other objectives such as grants, research or security initiatives.

This means that UNI holders – and delegates acting on their behalf – now manage something much closer to an operating budget and capital allocation plan. The quality of governance proposals, the transparency of reporting and the discipline in evaluating trade-offs will matter more than ever.

4.2 Risks and Opportunities of Treasury-Like Revenues

Whenever a decentralized organization controls meaningful revenue, there is a risk of short-term thinking. Proposals that sound attractive on social media may not always be the best use of funds for the protocol’s long-term health. UNIfication mitigates this by making the burn mechanism the default path for revenue: unless governance explicitly decides otherwise, value flows toward reducing supply rather than toward external spending.

At the same time, the existence of revenue opens the door to more ambitious initiatives. The DAO could, for example, choose to allocate a clearly defined share of income to a developer fund that supports tooling, security audits or integrations on Unichain and other supported networks. If such investments successfully grow usage, they can create a positive feedback loop: more activity, more fees, more burning and a stronger incentive for new participants to join the ecosystem.

5. What UNIfication Signals for DeFi Tokenomics

Because Uniswap is one of the most visible and battle-tested protocols in the industry, its choices often influence how other projects think about design. UNIfication sends several messages about where DeFi tokenomics might be heading.

5.1 The Era of Pure Governance Tokens Is Fading

In the previous cycle, many protocols launched tokens that served only as voting tools. Over time, markets discovered that it is difficult to maintain community engagement and long-term conviction when a token has no explicit link to the economic performance of the protocol. Such designs tend to rely heavily on narratives and expectations rather than measurable cash flows.

UNIfication does not turn UNI into a traditional yield-bearing asset, but it does provide a clear bridge between protocol usage and token supply. That bridge may become a widely copied pattern: tokens that remain primarily governance oriented but whose supply schedules are adjusted in response to real revenues, not just predetermined inflation and emissions.

5.2 Burning as a Shared Language Between Builders and Holders

Another notable aspect is how burning becomes a simple metric that both developers and investors can understand. When new initiatives such as Unichain or Uniswap v4 are proposed, community members can ask a straightforward question: how will this change the annual amount of UNI removed from circulation? Even if the answer is only an estimate, it gives people a way to compare projects and prioritize roadmap items based on expected impact.

For builders, this creates an incentive to design features and products that generate sustainable fee streams. For token holders, it offers a more concrete basis for evaluating governance proposals, beyond slogans or vague promises of growth.

6. Key Metrics to Watch After UNIfication

For anyone following UNI as an investment or Uniswap as infrastructure, UNIfication marks the beginning of a new monitoring regime. Several metrics are likely to become central to analysis over the coming quarters and years:

• Actual burn rate: How many UNI are being retired each month as a result of protocol fees, Unichain sequencer fees and any future revenue sources? Is the burn rate growing, stable or declining?

• Liquidity provider behavior: Do LPs remain comfortable supplying capital to pools where protocol fees are enabled, or does liquidity migrate to fee-free venues? Are any changes in fee structures offset by higher volumes and better capital efficiency?

• Governance quality: Are follow-up proposals around revenue and treasury management well researched and clearly presented? Do they include data and scenario analysis, or are they primarily driven by short-term sentiment?

• Role of Unichain and other expansions: As Uniswap grows beyond Ethereum mainnet, how much of the additional activity actually flows back into UNI burns? Are secondary networks complementary, or do they fragment liquidity and attention?

The answers to these questions will determine whether UNIfication ends up being remembered as a symbolic gesture or as the start of a more sustainable economic era for the protocol.

7. Conclusion: A Rare Case of a Leading Protocol Choosing the Community First

It is not common to see a major protocol voluntarily redirect revenue away from a private company and toward a shared, transparent mechanism controlled by the community. By activating protocol fees, burning a large portion of the treasury, setting interface fees to zero and linking Unichain revenues to UNI burns, Uniswap has taken a clear stance on how value should flow inside its ecosystem.

The new model is not guaranteed to solve every challenge. Balancing the interests of traders, liquidity providers, builders and token holders will remain an ongoing process. Governance needs to prove that it can handle greater responsibility without drifting into short-term decisions. Competitive pressures from other decentralized and centralized venues will continue.

Even so, UNIfication represents an important milestone in the broader story of decentralized finance. It illustrates that tokenomics is not static; it can be revised as protocols mature and as communities demand stronger alignment between usage and ownership. In that sense, Uniswap once again finds itself playing the role of a live laboratory for ideas about how decentralized systems can fund themselves while staying true to the goal of shared ownership.

Disclaimer: This article is for educational and analytical purposes only and does not constitute investment, legal or tax advice. Digital assets are volatile and may not be suitable for every investor. Always conduct your own research and consider consulting a qualified professional before making financial decisions.