Altcoins vs. Bitcoin: Why the Easy Outperformance Is Gone

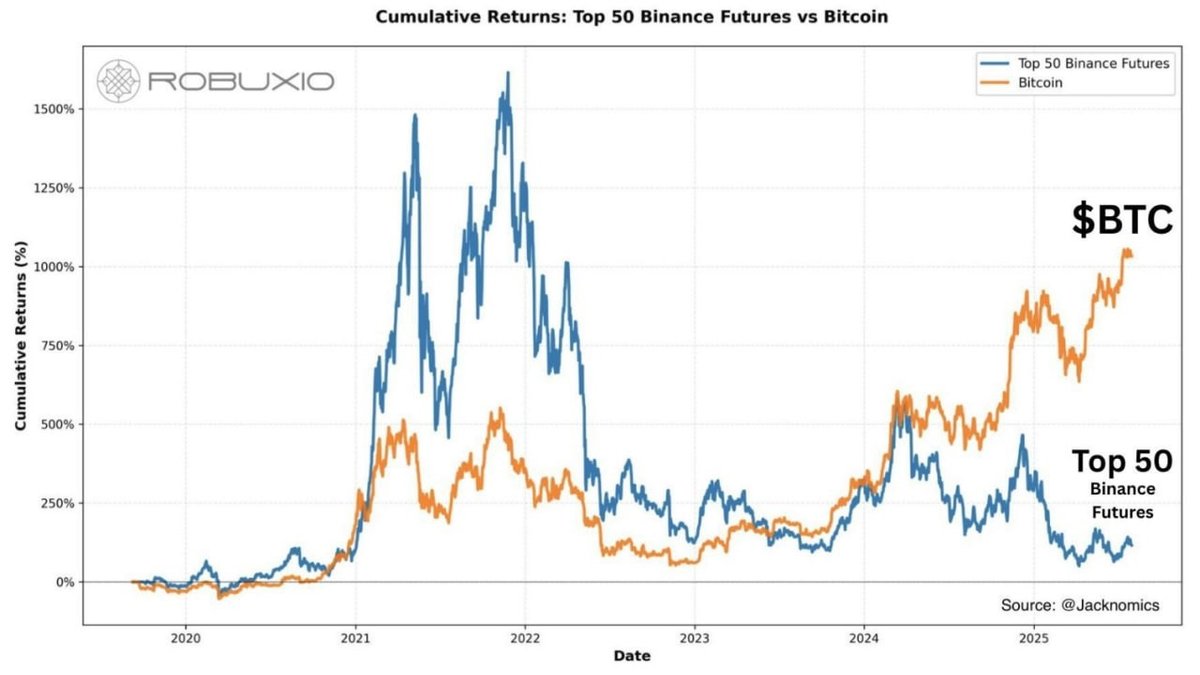

If you only joined the market in the last year, the chart might look surprising. It compares the cumulative returns of Bitcoin to an index of the top 50 Binance futures altcoins. In the 2020–2021 mania, the blue line (alts) soared far above the orange line (BTC). For a while, it felt almost trivial to beat Bitcoin simply by owning a basket of high-beta tokens.

Move your eyes to the right-hand side of the chart and the picture is flipped. As of 2025, Bitcoin has broken to new cumulative highs, while the altcoin basket has lagged badly, giving back most of its earlier outperformance. The story isn’t that all alts are dead—there are always a handful of strong outliers—but the default outcome for the average alt has shifted from “higher beta upside” to “structural underperformance.”

This article walks through what that chart is really telling us, why the environment for altcoins has become so unforgiving, and how to think more clearly about the question many traders are asking: if Bitcoin rips higher from here, how many alts will actually come along for the ride?

1. What the Chart Shows – and What It Doesn’t

The chart tracks cumulative percentage returns for two things over several years:

- Bitcoin (orange), treated as a buy-and-hold asset.

- An index representing the top 50 Binance futures altcoins (blue), rebalanced as the composition of top contracts changes.

During the 2020–2021 cycle, the blue line rockets far above the orange line. That era was dominated by DeFi summer, NFT mania, metaverse narratives and exchange incentive programs. Capital rotated aggressively across sectors, and new tokens had relatively small floats compared to their fully diluted valuations. In that context, a basket of alts behaved like a leveraged claim on Bitcoin’s uptrend.

After the peak, both lines trend downward as the entire market deflates—but the alt index falls much harder. What had been a 1,500% gain compresses brutally, while Bitcoin, despite deep drawdowns, retains a larger share of its cumulative return. Fast-forward to the most recent data: Bitcoin grinds back toward four-digit cumulative gains, whereas the alt index chops sideways and then drifts lower, struggling to stay meaningfully ahead of zero.

The chart is not telling you that no altcoin has done well. Individual names such as privacy coins, restaking plays, or new base layers can and do break away from the pack. The point is subtler: the average alt, inside a diversified futures basket, no longer offers a simple path to beating BTC. To do better, you have to pick the one or two horses that actually manage to run against the tide—a task that is increasingly difficult in practice.

2. Why Early-Stage Bull Markets Favoured Altcoins

To understand the change, it helps to recall why altcoins were so explosive in late 2023 and early 2024. In the first stages of a bull market, three forces tend to work in their favour:

1. Fresh narratives, limited float. New sectors—whether they are restaking, modular data layers or AI-linked tokens—launch with small liquid float relative to long-term supply. A modest amount of demand can move prices sharply.

2. Abundant risk appetite. Once Bitcoin establishes a strong uptrend, traders who missed the early move often chase higher beta alternatives. Leveraged products and aggressive yield programs amplify this demand.

3. Benchmark indifference. Early in the cycle, few managers are benchmarked to Bitcoin. Outperformance looks easy, and relative risk is downplayed in favour of absolute returns.

All of this was visible in the left and middle portions of the chart. As BTC broke away from the post-FTX lows, money rotated aggressively into alt sectors. Many of them did, in fact, deliver higher percentage returns than Bitcoin during that phase. The problem is that most of those moves were price first, fundamentals later—or never. When liquidity conditions changed and new supply hit the market, the lack of sustainable demand became obvious.

3. The New Headwind: Too Much Supply, Too Little Proof

In the current phase of the cycle, the altcoin complex faces a different set of structural forces:

• Unlocks and emissions. Large venture rounds and generous token incentives in 2021–2022 are now translating into steady selling pressure as early investors, team members and yield farmers gain liquidity. Even if user metrics improve, the market has to absorb a lot of new supply just to keep prices flat.

• Regulatory sorting. In several jurisdictions, crypto assets are being actively classified—as commodities, securities or something in between. Bitcoin sits in the clearest bucket; many altcoins do not. That uncertainty raises the hurdle for institutions considering anything beyond BTC and, to a lesser extent, ETH.

• ETF gravity. The arrival of spot Bitcoin and Ether ETFs has created a simple, compliant way for large pools of capital to get crypto exposure. That tends to benefit the two largest assets at the expense of the long tail.

• Higher standards for traction. After multiple boom–bust cycles, markets are less willing to pay high valuations for pure narratives. Questions about fees, users, security and treasury management arrive earlier in a project’s life.

The result is an uncomfortable reality for altcoin investors: the median project is not keeping up. A few standouts may attract attention with strong privacy tech, unique DePIN models or genuinely useful applications. The rest are stuck between early excitement and mature adoption, a zone where it is hard to justify persistent high valuations.

4. The Shift Toward Revenue and Narrative Quality

In earlier cycles, being "new" or "early" within a sector was sometimes enough. Today, the bar is noticeably higher. The market has begun to reward two types of altcoins:

1. Projects with durable revenue or clear economic flows. Protocols that can point to recurring fee income, real demand for blockspace, or meaningful non-token revenue (for example, software or infrastructure services) are better positioned. When buybacks or incentive programs are explicitly funded from revenue rather than from treasuries, investors are more willing to believe the economics are sustainable.

2. Assets with unusually strong narratives and attention. In a noisy environment, a few tokens manage to capture a disproportionate share of social and media mindshare—sometimes due to genuine innovation, sometimes due to cultural momentum. These are the "strong horses" that can move even when the rest of the pack is walking sideways.

An example often mentioned in trader chats is Zcash (ZEC). Regardless of one’s view on the asset, it illustrates a type of behaviour that stands out in the data: an older token with a clear narrative—privacy—periodically diverges from the rest of the market and stages independent rallies. That does not make ZEC a recommendation, nor does it guarantee future performance, but it shows the pattern: in a difficult environment for alts, only one or two names per sector may actually sprint.

For everyone else, the days of "buy a basket of whatever is new and wait" are over, at least for now. Without sustained fees, users and governance, the gravitational pull of Bitcoin’s relative strength eventually reasserts itself.

5. The Breadth Question: What Happens If Bitcoin Rips?

This brings us to the uncomfortable but important question: if Bitcoin rallies hard from here, how many altcoins will participate?

Historically, strong Bitcoin moves have tended to be followed by a period of "catch-up" as traders rotate into alts once BTC volatility slows. However, the chart suggests that the relationship is no longer automatic. Several factors could shape the breadth of the next move:

• Where the demand is coming from. If the next leg higher is driven primarily by ETF flows and treasury-style buyers, the incremental demand will be concentrated in BTC (and possibly ETH). Retail-driven surges, by contrast, tend to spill over into smaller names.

• How risk managers react. Many funds that were burned by 2022’s collapses have rewritten their mandates. For some, owning altcoins now requires a more explicit justification than owning Bitcoin. That can slow or limit rotation.

• Regulatory clarity for specific sectors. If certain categories—say, staking derivatives or DePIN tokens—receive clearer guidance, capital within those verticals may move more freely, even if broad altcoin indices lag.

• Unlock calendars and treasury practices. Projects facing heavy unlocks or aggressive treasury spending may see any BTC-led bounce sold into by insiders and team wallets, choking off potential rallies.

In practical terms, the answer to "how many alts will go up" is likely closer to "fewer than last time" than to "almost all of them." Breadth may still expand during euphoric phases, but the baseline expectation should be narrower participation, with more emphasis on quality and narrative differentiation.

6. Rethinking “Alt Season”

One of the most persistent memes in crypto is the idea of an inevitable "alt season"—a time when capital spills out of Bitcoin and lifts virtually every other token, almost regardless of fundamentals. The chart you’re looking at is a quiet argument against treating that meme as a law of nature.

Rather than asking when alt season will arrive, a more useful set of questions might be:

- Which sectors have clear, non-speculative use cases that could support multi-year demand for blockspace or protocol services?

- Which token designs align fees, users, and holders in a way that makes sense outside of a bull market?

- Which projects have governance processes capable of adapting tokenomics as conditions change, instead of being locked into unsustainable emissions?

- How concentrated is the ownership, and what does the unlock schedule look like over the next 12–24 months?

These questions are less exciting than the promise of a universal alt season, but they map more closely to how durable value is likely to be created in the current environment. They also highlight why a broad index of altcoins can underperform even when a few individual names are thriving: the index is dragged down by projects that never make it past the narrative phase.

7. Education, Not Prediction

It is tempting to treat a chart like this as proof that "Bitcoin is the only asset worth holding" or, conversely, that "altcoins are due for a monster catch-up." Both claims are overly confident. Markets are adaptive; the next few years will almost certainly contain sectors and tokens that are not yet on anyone’s radar.

The educational value of the chart lies elsewhere. It teaches at least three lessons:

1. Beta is not free. Higher volatility assets may outperform in the early part of a cycle but can underperform dramatically over a full cycle if supply, governance or demand conditions are weak.

2. Diversified baskets can hide structural decay. Owning an index of "top 50" futures sounds diversified, but if many constituents are short-lived narratives, the basket will trend lower once the music stops—even if a few stars shine.

3. Relative strength can flip. Bitcoin’s role in portfolios is evolving. As more institutional channels open, the relative balance between BTC and the alt complex can shift even without dramatic regulatory changes.

For students of the market, those lessons are more valuable than any short-term price call. They suggest that the skill ceiling for altcoin investing is rising: picking winners requires more work, more domain knowledge, and more attention to non-price metrics than in prior cycles.

8. A More Nuanced Way to Look Ahead

Where does this leave someone trying to make sense of the next phase of the cycle? A few balanced perspectives can help:

• Bitcoin remains the benchmark. Whether you invest in altcoins or not, BTC is the reference point. Understanding its role in institutional portfolios, ETF flows and state-level decisions (like the Texas reserve allocation) is essential context for any other trade.

• Altcoins are moving from “lottery tickets” to “early-stage equities”. Many of the questions investors now ask about alts—revenue, margins, user growth, regulatory footing—sound like equity research. That is a sign of maturation, but it also means the bar for investment is higher.

• Concentration of winners is likely to increase. If the chart’s trend continues, a small number of projects may capture an outsized share of attention and capital. The existence of a ZEC-like outlier does not guarantee the success of the group; it highlights its rarity.

• Risk management beats storytelling. Regardless of your view on Bitcoin versus alts, position sizing, diversification, and an honest assessment of downside scenarios matter more than the most compelling narrative.

In that sense, the real message of the chart is not that altcoins are over or that Bitcoin is destined to dominate forever. It is that the easy phase of the game is finished. The market is no longer paying simply for showing up with a token and a theme. It is beginning to ask harder questions, and the answers will determine which projects manage to escape the gravity of the average altcoin index.

This article is provided for informational and educational purposes only and does not constitute financial, investment, legal or tax advice. Nothing here should be interpreted as a recommendation to buy, sell or hold any digital asset, including Bitcoin, ZEC or any altcoin index. Digital assets are volatile and can involve a high risk of loss. Always conduct your own research and consider consulting a qualified professional before making financial decisions.