Strategy’s Latest $980M Bitcoin Purchase: Conviction, Concentration Risk, and What It Signals for the Market

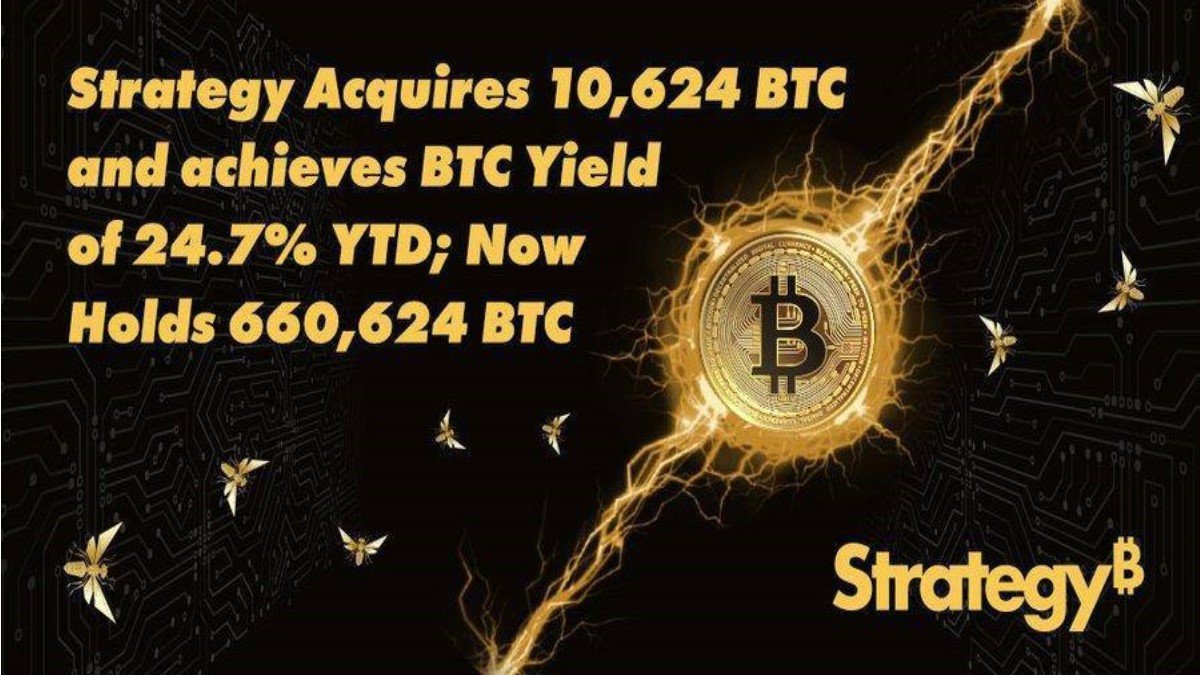

Another week, another nine-digit Bitcoin ticket from Strategy. According to the latest disclosure from Michael Saylor, the company has acquired 10,645 BTC for roughly 980 million USD, at an average price around 92,100 USD per coin. After this purchase, Strategy now holds 671,268 BTC. At a spot price close to 89,550 USD, that pile is worth approximately 60.1 billion USD, with an estimated average acquisition cost of about 75,000 USD per Bitcoin.

Those figures are striking on their own. But the deeper story is not just that one company continues to accumulate. It is how Strategy’s balance sheet has turned into a live laboratory for what happens when a listed corporation leans almost entirely into a single digital asset as its treasury reserve. The latest purchase is another data point in a multi-year experiment with far-reaching implications for corporate finance, market structure, and investor psychology.

1. From software vendor to de facto Bitcoin holding company

Strategy started life as an enterprise software business. The pivot began in 2020, when management decided that holding large idle cash balances in a negative real-rate world did not align with their long-term view on monetary policy. Instead of traditional short-term securities, they sought exposure to an asset with a capped supply and global liquidity. Bitcoin became the centerpiece of that thesis.

Over time, the firm raised capital via equity offerings and convertible debt, repeatedly deploying proceeds into additional Bitcoin purchases. With each acquisition round, the link between the company’s equity valuation and the underlying software business became weaker, while the link to the Bitcoin price became stronger. Today, with 671,268 BTC on the balance sheet, Strategy behaves, in many respects, like a leveraged Bitcoin operating company that happens to have a legacy software arm attached.

The new 10,645 BTC lot reinforces this identity. Importantly, Strategy did not wait for a deep market reset to buy. The purchase price (~92,100 USD) sits well above the company’s estimated average cost basis (~75,000 USD) and not far below the current trading range. That tells us something about how management views timing and valuation.

2. What this latest buy says about Strategy’s time horizon

Buying almost a billion dollars’ worth of Bitcoin near all-time-high territory is not a move aimed at capturing a small technical bounce. It reflects a time horizon measured in cycles, not quarters. From Strategy’s perspective, the key question is not whether Bitcoin is fairly priced this month, but whether it remains scarce and relevant ten years from now.

Several elements of the strategy stand out:

• Corporate-scale dollar cost averaging. Instead of making one massive, all-in purchase, Strategy has accumulated through dozens of tranches across multiple years. That approach smooths timing risk and keeps the company in the market regardless of short-term volatility.

• Acceptance of mark-to-market volatility. With an average cost near 75,000 USD and a spot price below 90,000 USD, Strategy is currently in profit on a book basis. But management has repeatedly signaled that they are comfortable with large, temporary drawdowns if the long-run thesis remains intact. In other words, accounting swings are treated as noise around a structural bet.

• Use of corporate tools to scale exposure. Equity issuance, debt offerings and, at times, creative financing structures have allowed the firm to expand its position well beyond what retained earnings alone would support. Shareholders, implicitly, sign up for that leverage when they own the stock.

The latest purchase therefore functions less as a market-timing signal and more as a credibility signal. Strategy is showing bondholders, equity investors and counterparties that its stated plan—to acquire and hold Bitcoin as a long-term reserve—is not just rhetoric. It is an operating rule.

3. A growing share of a finite asset

At 671,268 BTC, Strategy controls roughly 3–4% of the current circulating supply of Bitcoin, depending on the exact figure used for coins in free float. That is a notable share for a single listed corporation. When combined with the holdings of exchange-traded products, governments and other corporates, a significant slice of Bitcoin’s supply is now locked inside institutional balance sheets rather than sitting on retail trading venues.

This concentration has several consequences:

• Reduced immediate float. Large, buy-and-hold entities like Strategy do not typically churn their positions. As more coins migrate from exchanges to long-term treasuries, the pool available for day-to-day trading shrinks, potentially amplifying price moves when marginal demand spikes or fades.

• Higher sensitivity to corporate decisions. When a single company holds hundreds of thousands of coins, its internal decisions—whether to raise capital, pledge assets, or explore structured yield strategies—can affect market sentiment even if the underlying supply cap of 21 million remains unchanged.

• Growing policy relevance. Regulators and index providers have to consider whether such entities are primarily technology businesses, asset managers, or something in between. That classification informs how they are treated in benchmarks, capital rules and disclosure norms.

Strategy’s latest acquisition underlines how far Bitcoin has traveled from its early days as a niche experiment. A treasury reserve measured in tens of billions of dollars is not a hobby; it is a core corporate asset, intertwined with funding, governance and risk management decisions.

4. Benefits and risks for Strategy’s shareholders

For equity holders, Strategy offers a very particular proposition.

4.1. The upside: leveraged exposure and institutional rails

On the positive side, shareholders receive a form of leveraged Bitcoin exposure wrapped in a listed security. Investors who cannot or do not wish to hold coins directly—due to mandate constraints, operational limitations or simply preference—can gain exposure through a stock that trades on a major exchange, reports under standard accounting rules and is covered by mainstream research desks.

In addition, the company has been experimenting with ways to generate yield on part of its holdings, as reflected in references to a year-to-date Bitcoin yield in the mid-20% range. While the details of those activities matter greatly for risk, the broad idea is that a treasury of this size can potentially earn incremental returns by carefully structuring hedges, lending arrangements or other capital-markets transactions, all while maintaining a long directional bias.

4.2. The trade-offs: single-asset risk and funding dependence

The flip side is that Strategy has become highly concentrated. The company’s economic fate is now closely tied to one asset class and, in practical terms, one asset. That introduces several layers of risk:

• Price risk. A deep and prolonged Bitcoin drawdown would directly erode the value of the balance-sheet reserve, potentially pressuring covenants or limiting the ability to raise further capital on favorable terms.

• Funding risk. Many of Strategy’s acquisitions have been financed via markets that are open only when investor appetite is healthy. If conditions change, refinancing or new issuance could become more costly, slowing the pace of accumulation or forcing management to adjust strategy.

• Perception risk. Some institutional allocators view the stock as a proxy for Bitcoin itself; others see it as an operating business with an unusual treasury policy. These differing lenses can create volatility when short-term expectations diverge from management’s long-term narrative.

The latest 10,645 BTC purchase does not resolve these tensions; it amplifies them. For committed shareholders, the news aligns with the long-held promise: Strategy will continue to accumulate whenever it has dry powder. For more cautious observers, the question is whether the company is approaching the limits of how much single-asset exposure a listed corporation can responsibly carry.

5. Market structure: does Strategy’s buying still move the needle?

When Strategy first began its accumulation program, each new purchase announcement had a powerful psychological effect. The market was still getting used to the idea that a corporate treasurer would treat Bitcoin as a primary reserve asset. In today’s environment, with spot ETFs, sovereign holdings and a broader universe of institutional participants, individual announcements can feel less dramatic.

Yet the absolute numbers still matter. A 980 million USD order is large even by current market standards, particularly if executed patiently over the order book rather than via block trades with a single counterparty. The impact is not only in the immediate flow, but in the signal it sends to other boards, CFOs and risk committees:

• Proof of operational feasibility. Strategy has demonstrated that it is possible to integrate large-scale Bitcoin custody, accounting and disclosure into the life of a public company. That reduces the perceived operational barrier for others.

• Benchmark for risk tolerance. The company’s willingness to continue buying after significant rallies challenges the notion that corporates should only consider digital assets during deep bear phases.

• Reference point for market narratives. When Bitcoin is consolidating or pulling back, additional corporate purchases can be interpreted as a vote of confidence in the long-term thesis, even if they do not immediately reverse price trends.

That said, it is important to avoid overstating the direct cause-and-effect. Bitcoin’s daily trading volume across spot, derivatives and structured products runs into many billions of dollars. Strategy is a major long-term participant, but it is one participant among many. Its role is best understood as a structural buyer that periodically absorbs supply, not as a perpetual price anchor.

6. Lessons for other treasuries and individual investors

Strategy’s approach inevitably invites imitation. Some corporate leaders admire the simplicity of converting idle cash into an asset with a capped supply. Others are attracted by the publicity and share-price premium that a clear, high-conviction narrative can bring. But copying the playbook without context can be risky.

Several lessons stand out:

• Balance sheet strength matters. Strategy built its position over time, using a mix of equity and debt, while maintaining access to capital markets. A smaller company with limited financing options may not be able to withstand the same level of volatility.

• Time horizon must be aligned. Management, the board and key shareholders need to share a long-term perspective. If any group expects quick gains and becomes uncomfortable during drawdowns, the strategy can unravel at the worst possible moment.

• Risk disclosure should be explicit. Clear communication about how digital assets affect earnings, book value and potential downside scenarios is essential. Ambiguity can damage trust more than volatility itself.

• Diversification still has value. Even if a company believes strongly in Bitcoin’s long-run prospects, maintaining a mix of assets and revenue streams can provide resilience when markets move against that thesis for extended periods.

For individual investors, the main takeaway is that owning Strategy stock is not the same as holding Bitcoin directly. The equity carries additional layers of business risk, leverage and governance. Some may appreciate that bundle; others may prefer simpler exposure through regulated funds or self-custodied assets. Understanding those distinctions is crucial before making allocation decisions.

7. Where does this leave the broader Bitcoin narrative?

Strategy’s new purchase lands in a phase where Bitcoin has experienced a sizeable pullback from recent highs, even as institutional involvement continues to deepen through ETFs, tokenized products and corporate treasuries. In that environment, a near-billion-dollar buy is a reminder that, for some actors, the long-term story has not changed:

- Bitcoin remains a scarce asset with a transparent issuance schedule.

- Large, long-horizon investors are willing to hold through multiple cycles.

- Public companies can, with careful planning, integrate digital assets into traditional corporate structures.

None of this guarantees smooth price action or eliminates the possibility of deep corrections. What it does show is that Bitcoin is no longer solely the domain of individual traders reacting to short-term headlines. It is increasingly embedded in the treasuries of entities that think in decades.

8. Conclusion: conviction on display, questions still open

By adding 10,645 BTC at around 92,100 USD per coin, Strategy has once again made its priorities unmistakably clear. The company is prepared to allocate substantial capital to Bitcoin even when the asset is trading near the upper end of its historical range. With 671,268 BTC now on the balance sheet, valued at approximately 60.1 billion USD, Strategy has become one of the most concentrated and visible expressions of the digital-asset thesis anywhere in public markets.

For supporters, this is a powerful vote of confidence in Bitcoin’s long-term role as a digital reserve asset. For skeptics, it raises questions about concentration, corporate governance and the prudence of tying a listed company so tightly to a single, volatile asset.

Both perspectives can be true at the same time. What is clear is that Strategy’s actions continue to shape the conversation about how institutions engage with Bitcoin. Each new purchase reinforces that this is no longer a side bet—it is the core of the company’s identity. How that experiment plays out over the next decade will offer lessons not only for crypto markets, but for the future of corporate treasury management more broadly.

Disclaimer: This article is for educational purposes only and does not constitute financial, investment or legal advice. Digital assets are volatile and carry risk. Readers should conduct their own research and consult qualified professionals before making any investment decisions.