Silver at $70, GDP at 4.3%: Hard Assets Roar While Crypto Regroups

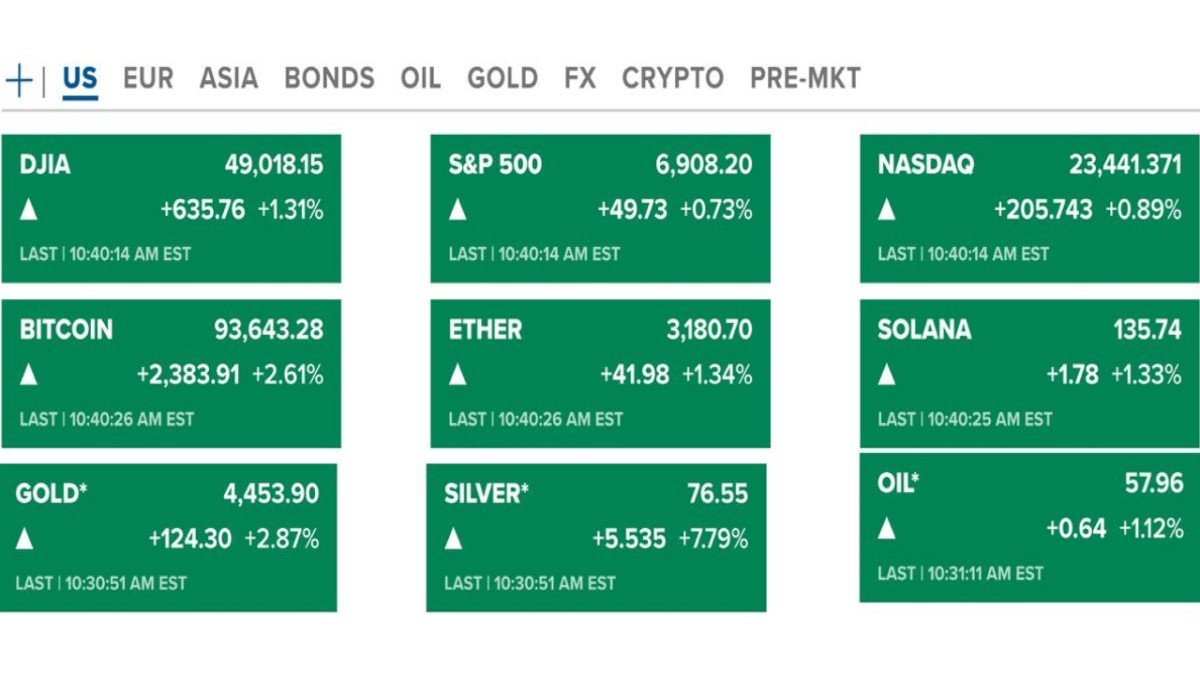

The past 24 hours have been a textbook example of how interconnected global markets have become. Silver has climbed to a fresh all-time high around 70 USD, gold has notched yet another record, the S&P 500 has closed at a new peak, and U.S. GDP for the third quarter has been revised up to 4.3%. At the same time, crypto continues to evolve beneath the surface: BitMine is adding tens of millions of dollars in ETH, new stablecoins are being minted, and both U.S. states and foreign central banks are reconsidering how ordinary savers can interact with digital assets.

This is not a simple “risk-on versus risk-off” story. It is a moment where hard assets, equities and digital assets are all trying to price the same underlying questions: how credible is the current policy mix, how scarce will safe collateral be over the next decade, and how deeply will tokenized markets integrate into the existing financial system?

1. Silver and gold send a loud signal about trust and duration

Silver breaking through 70 USD and gold trading near 4,500 USD are not just headline numbers; they are signals. Historically, precious metals have tended to outperform when investors worry about a combination of currency debasement, long-term fiscal pressure and geopolitical tension. What makes this episode unusual is that metals strength is happening alongside record equity prices and robust GDP growth rather than during an obvious downturn.

When both stocks and metals make new highs at the same time, one interpretation is that investors are diversifying their fear. Equities price in optimism about earnings, productivity and innovation. Gold and silver price in concern about the purchasing power of money and the long-run path of public debt. The fact that silver has now become one of the largest assets in the world by market value, even surpassing giants like Apple, underscores how much capital has rotated into the “store-of-value” narrative.

For crypto investors, there is an uncomfortable but useful parallel. Bitcoin is often described as “digital gold”, while some layer-1 and DeFi tokens function more like high-growth, high-beta tech equities. The dual breakout in metals and stocks suggests that markets are not yet being forced to choose between growth and safety; instead, they are paying a premium for both. The question for digital assets is whether they are viewed as closer to the gold side of that spectrum or the growth-equity side—and that answer may shift from cycle to cycle.

2. A 4.3% GDP print strengthens Trump’s policy narrative

The latest data show U.S. GDP growing at 4.3% in Q3, significantly above earlier forecasts. President Trump has quickly linked this performance to his tariff policies and fiscal framework, arguing that the numbers prove his approach is driving a new era of American strength. The message from the White House is clear: strong growth, resilient consumption and firm corporate profits are being attributed to higher trade barriers, targeted tax measures and assertive economic management.

From a macro perspective, the story is more layered:

• Consumption is the core driver. Household spending remains the backbone of the expansion, supported by wage income, wealth effects and targeted tax relief.

• Fiscal policy is highly supportive. Government spending and tax reductions together provide a sizeable demand boost, helping keep growth above what many economists view as the long-run potential rate.

• Trade and tariffs are a mixed influence. Tariffs can shift some demand towards domestic production and generate revenue, but they also raise input costs and can trigger counter-measures abroad. The net effect varies by sector and time horizon.

What matters for markets is not only the current growth rate, but how it interacts with the next big decision: who will lead the Federal Reserve. President Trump has stated that he will only appoint a Fed Chair who is willing to cut interest rates and to align closely with the administration’s economic direction, even going so far as to say that “anybody that disagrees with me will never be the Fed Chairman.”

This increases policy uncertainty in an unusual way. On one hand, investors hear promises of lower future rates and ongoing fiscal push—both supportive for asset prices. On the other hand, they see the possibility of reduced central-bank independence, which can undermine confidence in the long-term stability of the currency and bond market. Precious metals seem to be reacting to that second concern, while equities appear more focused on the near-term growth impulse.

3. Tax and regulatory fronts: Arizona, Russia and a “Golden Age” narrative

Beneath the headline GDP and Fed stories, regulatory and tax details are slowly reshaping the crypto landscape.

In the United States, Arizona is exploring ways to ease the tax burden on crypto users. While details are still emerging, the general thrust is to make it less cumbersome for residents to hold and transact digital assets, potentially through exemptions or simplified capital-gains treatment for smaller transactions. This sits alongside efforts in Congress to create exemptions for low-value stablecoin payments, reducing the paperwork burden on everyday use.

Internationally, the Bank of Russia is considering allowing non-qualified (retail) investors to purchase crypto under certain conditions. For years, Russian authorities have taken a cautious stance, focusing on systemic risk and capital controls. Allowing broader access—even with restrictions—would mark a notable shift, acknowledging that digital assets are now part of the mainstream financial conversation rather than a niche speculation.

Overlaying all of this is a more aggressive public narrative from U.S. officials responsible for digital-asset policy. The U.S. “crypto czar” David Sacks has described the current moment as a “Golden Age” for the sector, referencing the combination of clearer legislation, institutional adoption and the rise of tokenized real-world assets. Whether markets entirely agree with that label is debatable, but it captures the mood among policymakers who see crypto as infrastructure rather than a side-show.

4. Capital flows: ETH accumulation, stablecoin expansion and Solana's treasury story

At the protocol level, the flow of real capital tells its own story about conviction and positioning.

First, BitMine, chaired by Tom Lee, has just added roughly 88.1 million USD worth of ETH to its balance sheet. This purchase comes on top of prior accumulation that already placed the firm among the largest corporate holders of Ethereum. For long-term observers, it reinforces three points:

- ETH is increasingly being treated as a strategic reserve asset by specialized firms, similar to how certain publicly listed companies treat Bitcoin.

- Staking yield and collateral utility matter. BitMine’s business model depends not only on price appreciation, but also on using ETH for staking, collateralized lending and structured products.

- Corporate time horizons differ from retail cycles. When individuals are debating short-term pullbacks, treasury-style buyers often focus on multi-year theses and the cumulative effect of future protocol upgrades.

Second, stablecoins continue to grow quietly in the background. Roughly 500 million USDC has been freshly issued, signalling that institutional and retail demand for regulated, dollar-linked tokens remains robust. New issuance can reflect many things—on-ramping of fresh capital, migration from other stablecoins, or preparations for year-end payments—but in every case, it underscores that stablecoins have become core infrastructure for both CeFi and DeFi.

Third, the Solana ecosystem is carving out a distinct role as a high-performance platform for treasury strategies. Upexi, a SOL reserve company, has filed to raise up to 1 billion USD and currently holds about 2 million SOL, worth roughly 248 million USD at recent prices. Alongside this, Coinbase has enabled SOL deposits and withdrawals via the Base network, tightening the connection between Solana liquidity and the broader Ethereum L2 environment. Together, these moves highlight how layer-1 ecosystems are no longer just about blockspace for apps; they are becoming balance-sheet decisions for corporates and exchanges.

5. Market structure stress: frozen wallets, MEV controversy and the cost of opacity

Not all of today’s stories are constructive. Some of the sharpest lessons are coming from places where infrastructure and incentives collide.

On the WLFI side, a wallet address reportedly associated with Justin Sun has been blocked from transacting, with on-chain data suggesting that assets worth tens of millions of dollars are now effectively frozen. Regardless of the specific personalities involved, the episode illustrates two important points:

- Control points still exist in supposedly open systems. Gateways, bridges and protocol-level permissions can be used to restrict movement of funds when legal, compliance or governance triggers are met.

- Users must understand where trust re-enters the stack. Even on public chains, interactions with permissioned protocols or wrapped assets often reintroduce elements of centralised control.

In parallel, Pump.fun has been hit by allegations of insider-favoured MEV activity, with some market participants claiming that preferential access or aggressive execution strategies have led to large losses for ordinary traders—running into billions of dollars when aggregated across many small events. The details are still being debated, but the broader lesson is clear: as on-chain markets become faster and more complex, execution quality and fairness become as important as token design.

Neither episode should be interpreted as a verdict on the entire sector. Instead, they serve as reminders that market-structure risk is real: orderflow, MEV, permissions and governance can materially influence outcomes even when base-layer cryptography is sound. For long-term participants, that means:

- Taking time to understand how an exchange, DEX or protocol handles order routing and MEV.

- Recognising that “on-chain” does not automatically mean “neutral and fair” in every dimension.

- Valuing transparency, clear documentation and independent audits as part of the due-diligence process.

6. How all of this fits together for crypto investors

Putting silver at 70, GDP at 4.3%, BitMine’s ETH purchase, USDC issuance and the latest governance controversies into one picture, three themes stand out.

6.1 Hard assets and digital assets are rhyming, not competing

The surge in silver and gold is often portrayed as a challenge to Bitcoin’s “store-of-value” narrative. In reality, these moves can coexist and even reinforce each other. All three—gold, silver and Bitcoin—benefit when investors question the long-run trajectory of fiat currencies and public debt. If anything, metals strength can be seen as a macro confirmation that scarcity premiums are back in fashion. The key difference is that metals sit inside the traditional custody and derivatives system, while Bitcoin lives on an open, programmable ledger.

6.2 Policy is becoming more directional and more personal

President Trump’s comments about only appointing a Fed Chair who fully aligns with his views, and his assertion that tariffs are responsible for the “great economic numbers”, are signals that economic policy is increasingly anchored in personal commitments rather than purely technocratic processes. For markets, this reduces predictability: the path of rates, regulation and fiscal policy can swing more sharply depending on individual appointments.

For crypto, this cuts both ways. A leadership team that is open to digital assets and tokenized markets can accelerate integration into the mainstream. But a more personalised policy regime also increases headline risk and the possibility of sudden shifts in regulatory tone. That is why rules-based legislation—on market structure, stablecoins and taxation—remains crucial; it creates a floor of predictability beneath the day-to-day soundbites.

6.3 On-chain finance is maturing, but not evenly

The juxtaposition of BitMine quietly accumulating ETH and USDC adding half a billion dollars in supply with the WLFI and Pump.fun episodes highlights the uneven pace of maturation. Some corners of the market are starting to look like institutional-grade infrastructure, complete with treasury policies, audited reserves and integration into corporate workflows. Other corners still resemble experimental arenas where incentives are sharp, information is uneven and protections are limited.

For long-term investors, the educational takeaway is not to avoid experimentation altogether but to segment risk clearly: treat core assets (BTC, ETH, major stablecoins) differently from small-cap tokens, experimental DEX features or highly reflexive memecoins. The same way a traditional portfolio distinguishes between sovereign bonds, blue-chip equities and frontier markets, crypto portfolios benefit from explicit tiers of risk and time horizon.

7. Practical educational takeaways

Looking at the last 24 hours as a case study, a few practical lessons emerge for anyone trying to understand the intersection of macro and crypto:

• Macro data sets the background music, not the exact trading rhythm. A strong GDP print, record metals and new equity highs tell you something about the environment, but they do not dictate the next candle on a four-hour chart.

• Policy narratives matter as much as policy actions. When leaders publicly link growth to tariffs and promise future rate cuts, markets price not only current numbers but also perceived constraints on future decisions.

• Capital allocation by specialised firms is a slow, powerful signal. When entities like BitMine accumulate ETH or corporates raise capital to hold SOL treasuries, they are expressing multi-year conviction that can outlast short-term volatility.

• Stablecoin issuance is a barometer for on-chain activity. Fresh USDC supply does not guarantee price appreciation for risk assets, but it suggests that the plumbing for digital dollars is still expanding.

• Infrastructure risk is real, even without protocol failures. Wallet freezes, MEV controversies and governance disputes can affect outcomes without any cryptographic bug. Due diligence must therefore cover both code and human incentives.

Conclusion: reading the signals without overreacting

Silver at 70 USD and gold at record highs tell us that investors are willing to pay a premium for scarcity. A 4.3% GDP print tells us that the U.S. economy remains surprisingly strong under a highly active fiscal and trade regime. New ETH purchases, fresh USDC issuance and expanding Solana treasuries tell us that on-chain finance is moving further into the institutional arena. Meanwhile, wallet freezes and MEV disputes remind us that the road to a mature, fair digital market structure is still under construction.

For participants in crypto and traditional markets alike, the challenge is to integrate these signals without being whipsawed by every headline. Strength in hard assets does not automatically mean collapse in digital ones; strong GDP does not eliminate long-term concerns about debt; and regulatory progress does not remove the need for individual responsibility.

In that sense, the most constructive stance is both humble and prepared: recognise that we are in a rare period where macro, policy and technology are all shifting at once, and build portfolios, risk frameworks and learning habits that can survive more than one kind of future.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment, legal or tax advice. Digital assets and other investments carry risk and can be volatile. Always conduct your own research and consult a qualified professional before making financial decisions.