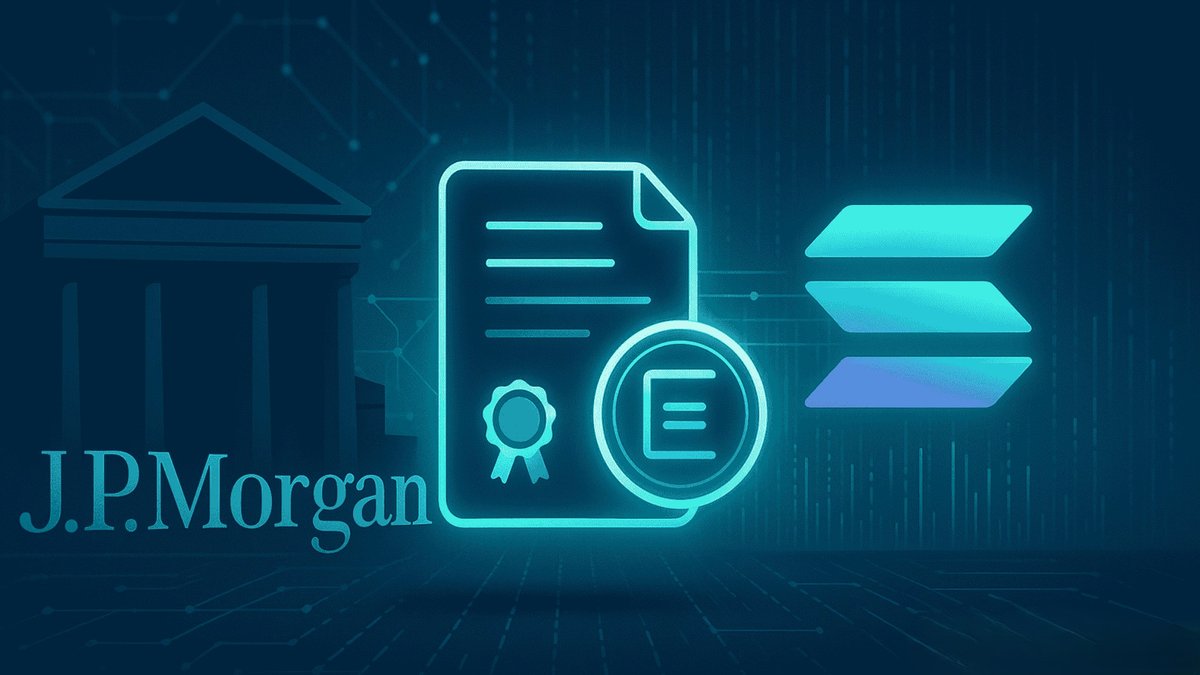

J.P. Morgan Runs Real Commercial Paper on Solana: Why This Deal Matters More Than the Headline

A few years ago, the idea that the largest bank in the United States would execute a real short-term funding deal on a public blockchain would have sounded like a thought experiment. Yet that is exactly what has just happened. J.P. Morgan has helped Galaxy Digital create and sell a short-term bond fully represented on Solana, with investors funding the purchase in stablecoins and Galaxy committing to repay in the same way.

On the surface, this looks like a niche event: one commercial paper transaction in a market that usually handles hundreds of billions of dollars through traditional channels. But at a structural level, it is an important signal. It shows that large banks are no longer treating blockchains only as a laboratory for internal pilots or private networks. They are beginning to use public infrastructure to move actual money and securities between real clients.

1. What J.P. Morgan and Galaxy actually did

To understand why this matters, it helps to unpack the mechanics. Galaxy Digital wanted to raise short-term funding, the kind of corporate borrowing that is typically done through commercial paper. Traditionally, that process involves dealer banks, clearing systems, custodians and settlement windows that operate only during business hours.

In this case, J.P. Morgan structured an on-chain version of commercial paper. Instead of issuing a conventional note through legacy systems, they created a tokenised instrument on Solana that represents Galaxy’s short-term obligation. Investors subscribed to the issue using a regulated stablecoin, and Galaxy will repay principal and interest in that same token at maturity.

From a legal perspective, the deal still sits inside the established framework of commercial paper. It has an issuer, a maturity date, a defined coupon and the usual documentation. The innovation is where and how the instrument lives: on a public blockchain, in a form that can settle almost instantly and be integrated into other on-chain applications.

2. A quick primer: what is commercial paper and why is it important?

Commercial paper is one of the quiet workhorses of modern finance. It is a form of short-term unsecured debt that companies use to cover working capital needs: paying suppliers, rolling inventories, bridging cash flows between receivables and expenses. Maturities are usually measured in days or weeks rather than years.

For large, creditworthy firms, commercial paper is cheaper and more flexible than bank loans. For investors such as money-market funds, it offers a way to earn a modest yield on short-duration assets. Although it rarely appears in headlines, this market plays a central role in keeping day-to-day corporate funding and cash management functioning smoothly.

Historically, however, commercial paper has been operationally complex. Issuances and settlements run through a tangle of registrars, central securities depositories, dealer networks and payment systems that do not operate 24/7. Documentation and reconciliation can take time. Cross-border deals add layers of currency and settlement risk.

An on-chain commercial paper instrument changes that equation. If issuance, ownership and settlement are represented on a shared ledger, much of the operational burden can be automated. That is the broader experiment J.P. Morgan and Galaxy are running on Solana.

3. Why a public chain, and why Solana?

For years, large financial institutions explored blockchain mainly through permissioned networks — controlled environments where only selected participants can run nodes. Those systems were useful for proofs of concept but often failed to achieve the network effects of public blockchains.

In this transaction, J.P. Morgan chose Solana, a public chain known for high throughput, low transaction fees and fast finality. From a purely functional standpoint, those characteristics are attractive for high-volume, low-margin operations such as short-term funding and settlement. A commercial paper desk cares about predictable execution, low cost and the ability to move funds quickly; Solana was designed with those requirements in mind.

The choice is also symbolic. By using a public network, J.P. Morgan is acknowledging that open infrastructure can be robust enough for regulated finance, provided that the integration layer (legal agreements, compliance, key management, risk controls) is built to institutional standards. In other words, the bank is not embracing every aspect of crypto culture, but it is willing to use the technology where it creates clear efficiency gains.

4. Stablecoins as the settlement asset

Another crucial detail is the use of stablecoins for both subscription and repayment. Investors bought the tokenised commercial paper using a stablecoin, and Galaxy will return funds in the same token at maturity. That choice transforms the stablecoin from a trading tool on exchanges into a settlement asset for real corporate borrowing.

This has several implications:

- 24/7 settlement. Stablecoin transfers are not limited by banking hours. Deals can settle in minutes at any time of day, reducing counterparty and settlement risk.

- Integrated cash and collateral. The same token can serve as a cash equivalent in one context and as collateral in another, simplifying treasury operations for both issuers and investors.

- Cross-border flexibility. For international investors, holding a regulated dollar-linked stablecoin may be operationally easier than opening accounts with multiple correspondent banks.

For regulators, this evolution also raises questions. Once stablecoins are accepted as a settlement medium for mainstream financial contracts, their design and oversight become critical. That is why so many regulators — from the UK’s FCA to US agencies and Asian authorities — are working on specific frameworks for tokenised money. The J.P. Morgan–Galaxy deal will likely be studied closely as an early example of how such instruments behave in practice.

5. From experiments to financial plumbing

J.P. Morgan has been exploring blockchain for years through its Onyx initiative, building systems for intraday repo, tokenised deposits and cross-border payments. Many of those projects used permissioned networks. What is new here is the deliberate step into a public chain carrying a real, externally funded security that sits within an established market.

This is a shift in how incumbents are using crypto infrastructure. Instead of asking whether a token will replace traditional finance, banks are asking how public networks can become invisible infrastructure inside existing products. Clients may still see a familiar term sheet and risk profile; they simply gain faster settlement and more flexible collateral management under the hood.

If this model scales, the market could see more instruments that look traditional on the surface — repos, certificates of deposit, money-market instruments — but are issued, traded and settled on public chains. Crypto, in that sense, becomes less of a separate asset class and more of a back-end technology for the broader financial system.

6. What this means for Solana and other public networks

For Solana, the transaction is an important validation of its long-term narrative as a high-performance execution layer for both digital-native and traditional assets. The chain has already hosted stablecoins, decentralised exchanges and consumer applications. The entrance of a large US bank with a real commercial paper deal signals that Solana’s performance profile is now being taken seriously by institutions as well.

That does not mean every future tokenised security will live on Solana. Different banks and issuers may choose different chains based on technical preferences, regulatory comfort and ecosystem tools. But the precedent matters: if the largest US bank is comfortable executing on a public chain once, it becomes easier for others to justify doing the same, whether on Solana, Ethereum, or other networks built with institutional use in mind.

7. Benefits for issuers, investors and intermediaries

Viewed through an educational lens, this deal illustrates several practical benefits of tokenisation.

7.1. For issuers like Galaxy

- Faster access to funding. Issuances can be structured and settled quickly, allowing treasurers to react to market conditions in near real time.

- Programmatic lifecycle management. Coupon payments, maturity redemptions and even roll-overs can be encoded into smart contracts, reducing manual processing and the risk of operational errors.

- Broader investor reach. On-chain instruments, once fully regulated, could in principle be accessible to a wider range of vetted investors through digital platforms, without depending on a single dealer channel.

7.2. For investors

- Transparent ownership. Holdings are visible on-chain, and settlement occurs in near real time, reducing reconciliation issues.

- More flexible collateral. Tokenised commercial paper could be pledged in other on-chain transactions, such as repo or margin funding, without complex re-papering.

- Operational efficiency. Using stablecoins for subscription and redemption can simplify cash management, especially for investors already active on digital-asset platforms.

7.3. For intermediaries like J.P. Morgan

- New service lines. Banks can position themselves as arrangers, custodians and risk managers for tokenised instruments, earning fees while leveraging their existing credit expertise.

- Better use of infrastructure. Integrating blockchains into their stack can reduce reliance on multiple legacy systems and cut settlement frictions.

8. Risks and open questions: regulation, resilience and interoperability

A balanced analysis has to acknowledge the open questions that come with moving sensitive financial contracts onto public chains.

• Regulatory clarity. Even when a specific deal complies with existing securities and payments rules, supervisors will be watching closely to ensure that systemic risk does not build up through new channels. Questions remain about how tokenised money and securities are treated in stress scenarios and how investor protections apply across jurisdictions.

• Operational resilience. Public networks are designed to be robust, but they are not immune to outages or technical incidents. Institutions must plan for contingency arrangements: what happens if a chain pauses, or if transaction costs spike unexpectedly?

• Interoperability. If different banks issue tokenised instruments on different chains, fragmentation could emerge. Cross-chain standards, custodial solutions and messaging layers will be needed to ensure that liquidity is not trapped in isolated silos.

• Data privacy. Public ledgers are transparent by design. Structuring deals in a way that protects sensitive counterparty information, while still allowing regulators and auditors to observe flows, requires careful design.

None of these challenges are insurmountable, but they underscore why tokenisation in regulated markets moves gradually. Each successful pilot expands the comfort zone of both regulators and institutions, while highlighting the safeguards that need to be strengthened before scale is possible.

9. From speculative narrative to institutional infrastructure

For the broader digital-asset ecosystem, the J.P. Morgan–Galaxy Solana transaction marks another step in a slow transition. The early years of crypto were dominated by narratives about rapid gains and headline price targets. Increasingly, however, the story is shifting toward infrastructure and utility: how blockchains can shorten settlement cycles, reduce operational risk and enable new forms of programmable finance.

That shift does not eliminate volatility or uncertainty, but it broadens the conversation. When the largest US bank is comfortable running a real funding deal on a public chain, it signals to other institutions that crypto technology is not only about new assets; it is about improving the way familiar assets are issued and moved.

In that sense, the most important outcomes of this experiment may be invisible to the public. If tokenised commercial paper becomes routine, treasurers will simply experience faster settlements and more flexible tools. Money-market funds might enjoy smoother operations. Investors may never think about the underlying chain. The network becomes part of the background — which is exactly how foundational infrastructure tends to succeed.

10. Key takeaways for readers

Several practical lessons emerge from this episode:

- Tokenisation is moving beyond slide decks into live transactions involving blue-chip institutions and real cash flows.

- Stablecoins are evolving from trading tools into settlement assets for mainstream financial contracts.

- Public chains like Solana are increasingly viewed as credible venues for regulated finance when combined with institutional-grade controls.

- The long-term impact is likely to be felt more in the efficiency of financial plumbing than in dramatic overnight changes. Incremental adoption can still reshape the system over time.

For now, the J.P. Morgan–Galaxy deal is one transaction in a huge market. But it offers a preview of a future where the distinction between “crypto” and “traditional finance” becomes less about asset type and more about the rails those assets run on. In that future, public blockchains are not a parallel universe; they are part of the wiring that quietly keeps global finance moving.