From 'Do Not' to 'Do It Safely': The Fed Rewrites Its Innovation Playbook for Banks

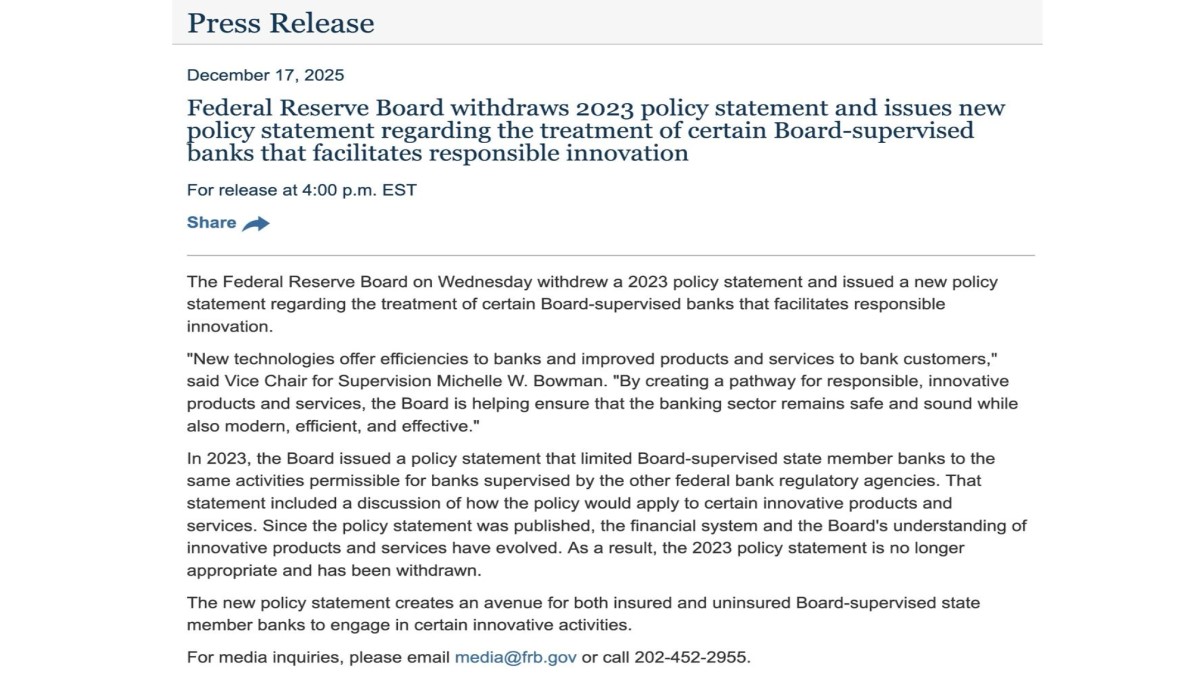

The Federal Reserve Board has quietly taken an important step in how it oversees innovation in the U.S. banking system. In a new policy statement released in December 2025, the Fed withdrew its 2023 guidance that had constrained the activities of Board-supervised state member banks and replaced it with a framework that explicitly encourages responsible, well-managed experimentation.

Vice Chair for Supervision Michelle W. Bowman summed up the new posture by emphasising that modern technologies can bring efficiency and better services to bank customers, and that the Board wants the sector to remain safe and sound while also modern and effective. In practical terms, the Fed is shifting from an implicit message of “don’t do anything your peers are not already doing” toward a more constructive question: “show us how you plan to do it safely.”

For banks, fintech partners and the broader digital-asset ecosystem, this is more than a technical regulatory tweak. It signals that the main U.S. prudential supervisor is ready to treat innovation as something to be channelled and governed, rather than something to be avoided by default.

1. What Exactly Did the Fed Change?

To understand the importance of the new statement, it is useful to recall what the 2023 guidance did. That earlier policy effectively said that state member banks supervised by the Fed could only engage in certain novel or complex activities if those activities were already permissible for banks overseen by other federal regulators, such as the Office of the Comptroller of the Currency (OCC) or the Federal Deposit Insurance Corporation (FDIC).

On paper, this was framed as an attempt to keep the regulatory playing field level. In practice, it tended to produce a “wait until someone else moves first” dynamic. If another agency had not yet clearly allowed a specific product or service, Fed-supervised banks were effectively discouraged from touching it, even if they believed they could manage the risk. That made it harder for state member banks to be first movers in areas like advanced payment technologies, tokenization of assets, or new forms of digital custody.

According to the new press release, the Board now believes that the financial system and its own understanding of innovative products have evolved to the point where the 2023 framework is no longer appropriate. As a result, the earlier document has been withdrawn and replaced with updated guidance that opens a clearer avenue for innovation by both insured and uninsured state member banks under Fed supervision.

2. A Shift in Supervisory Philosophy: From Restriction to Risk-Based Engagement

The most important change is not a specific permission, but a change in tone. The new policy statement is built around the idea of “responsible innovation.” Rather than treating new technologies as outliers that should be discouraged unless they perfectly match existing activities, the Fed is signalling that it is prepared to work with banks that want to explore new business models — provided they can demonstrate strong risk management, consumer protection and compliance.

This represents a notable shift in supervisory philosophy:

- Old framing: Innovation is suspected by default; banks must prove that anything new is essentially the same as what has already been allowed elsewhere.

- New framing: Innovation is recognised as inevitable and potentially beneficial; the key question is whether a bank can show that it understands the risks and has credible controls.

For bank management teams, that difference matters. A policy environment that begins with 'no' encourages minimal experimentation and pushes more ambitious projects into less regulated corners of the financial system. A framework that begins with 'show us your plan' encourages thoughtful pilots, robust governance and earlier engagement with supervisors.

3. What Counts as “Innovative” Today?

The Fed’s statement is deliberately technology-neutral. It does not list specific products or endorse particular vendors. Instead, it refers broadly to “innovative products and services” that may use new technologies or business models. In the current environment, that can cover a wide spectrum of activity, including:

• Advanced payment systems, such as real-time cross-border transfers, programmable payments or new merchant solutions.

• Tokenized representations of traditional assets, including deposits, money-market fund shares or other financial instruments that can be recorded and transferred on distributed ledgers.

• Data-driven credit and risk analytics, where banks use machine learning or alternative data to evaluate borrowers and manage portfolios.

• Embedded finance partnerships in which banking services are delivered through technology platforms or non-bank brands.

• Digital-asset-related services, such as custody, settlement or execution support for clients that hold cryptoassets, stablecoins or tokenized securities, subject to existing laws and regulations.

Each of these areas carries distinct operational, legal and reputational risks. What the Fed is saying is not that these activities are automatically appropriate, but that there is now a clearer pathway for banks to explore them within a supervised environment.

4. What the New Policy Means for Fed-Supervised Banks

For both insured and uninsured state member banks, the new statement offers two main benefits: regulatory clarity and procedural flexibility.

4.1 Reduced uncertainty

Under the withdrawn 2023 guidance, some banks worried that even well-designed innovation projects might be viewed skeptically simply because they were new. This created a “chilling effect”, where compliance and legal teams advised against proposals that could draw supervisory scrutiny, even if the risk was manageable.

The new policy softens that effect by making it explicit that innovation is acceptable in principle as long as it remains consistent with safety and soundness. That reduces the fear that trying something new will automatically be seen as stepping out of line. Instead, the emphasis is on doing the homework upfront: analysing risk, investing in controls, and engaging early with supervisors to discuss the approach.

4.2 A more flexible pathway

The Board also notes that the financial system has changed since 2023. Banks operate in a world where technological change is rapid and where customers increasingly expect their financial institutions to match the convenience and speed of digital-native firms. A rigid “follow someone else’s template” approach is not well suited to that environment.

By opening an avenue for both insured and uninsured state member banks to undertake innovative activities, the Fed is giving these institutions more room to design services that fit their specific business models. At the same time, the new policy keeps the familiar supervisory guardrails in place. Banks are still expected to:

- Maintain strong capital and liquidity positions.

- Demonstrate robust governance, with board-level oversight of major innovations.

- Comply with consumer-protection, anti-money-laundering and sanctions rules.

- Protect data and ensure operational resilience, including cyber security.

Innovation is therefore not a shortcut around regulation; it is an area where traditional risk disciplines are applied to new technologies.

5. Implications for Digital Assets and Tokenization

Although the Fed’s press release does not single out digital assets, the timing is notable. Over the past two years, banks, asset managers and payment companies have accelerated their work on tokenized deposits, stablecoins, and blockchain-based settlement systems. Other U.S. agencies, including the OCC and FDIC, have provided varying degrees of guidance on how banks can interact with these technologies.

The withdrawal of the 2023 policy removes an obstacle that effectively told Fed-supervised state member banks to avoid being early adopters in such areas. Under the new framework, a bank that wishes to, for example, use tokenized deposits for wholesale payments, support clients who settle trades using tokenized money-market funds, or offer carefully structured digital-asset custody services has a clearer route to make its case.

That route will still involve detailed supervisory discussions. Banks will need to explain how they manage operational risk, how they segregate customer assets, how they prevent misuse of platforms, and how they respond to incidents. But the starting assumption is no longer that such activity is off-limits simply because it is new.

For the broader crypto and tokenization ecosystem, this matters because large banks act as bridges between traditional capital markets and on-chain infrastructure. When banks are able to experiment, they can bring their risk culture, compliance frameworks and large balance sheets into the mix, potentially making emerging technologies more accessible to institutional clients in a controlled way.

6. The Competitive and Global Context

The Fed’s updated stance does not exist in isolation. Around the world, central banks and regulators are wrestling with how to balance financial stability against the need to keep their banking sectors competitive and innovative.

In Europe, regulators have been working on frameworks for tokenized securities, digital-euro experiments and open-banking standards. In parts of Asia and the Middle East, authorities are encouraging banks to explore real-time cross-border payments and tokenized assets within defined regulatory sandboxes. U.S. banks increasingly operate in this global environment and risk falling behind if domestic rules are perceived as too restrictive.

At the same time, non-bank firms — from fintech start-ups to large technology companies — have been offering financial services without carrying full banking charters. While these firms are subject to their own sets of rules, they can sometimes move faster in experimenting with new customer experiences. If regulated banks are kept on the sidelines, innovation does not stop; it simply migrates elsewhere.

By updating its guidance, the Fed is signalling that it wants banks themselves to be active participants in the next wave of financial innovation. The underlying message is that the safest place for experimentation is often within supervised institutions that have experience managing risk, rather than in unregulated corners of the market.

7. What Banks Need to Do Now

The new policy statement is not a free pass. It is an invitation to do more serious homework. Banks that wish to take advantage of the more open stance will need to invest in the foundations that make responsible innovation possible.

Key practical steps include:

• Strengthening governance: Boards and senior management should clearly define their risk appetite for innovative activities and ensure that there is a documented decision-making process for approving new products.

• Enhancing risk assessment frameworks: Traditional credit and market-risk tools may not fully capture the specific risks of digital platforms, tokenized instruments or complex third-party relationships. Banks will need tailored methodologies for assessing technology, operational and legal risk.

• Improving data and monitoring: Innovation often produces new types of real-time data. Using that data effectively — for example, to monitor transaction patterns, system performance or client behaviour — will be central to demonstrating that activities remain under control.

• Managing third-party risk: Many innovative products involve partnerships with technology vendors, cloud providers or fintech platforms. Supervisors will look closely at how banks oversee these relationships, including contractual safeguards, contingency planning and exit strategies.

• Prioritising consumer and investor protection: Clear disclosures, fair pricing and robust complaint-handling processes are essential, especially when products are complex or unfamiliar to end users.

In short, the Fed is encouraging innovation that is anchored in the same disciplines that have long underpinned safe banking: strong governance, conservative risk management and transparent communication.

8. How Investors and Market Participants Might Read the Signal

For investors who follow banks and digital-asset markets, the new policy statement sends several important signals:

• Regulatory risk is evolving, not disappearing. Banks may have more room to innovate, but they will still face close supervisory scrutiny and must allocate resources to compliance and risk management. This is not a deregulation wave; it is a recalibration.

• Innovation may increasingly take place inside the banking perimeter. As the Fed becomes more comfortable with experimentation, some activities that previously occurred primarily at non-bank firms may migrate into or be replicated by banks, potentially changing the competitive landscape.

• The long-term trend favours integration between traditional finance and new technology rails. Tokenized assets, real-time payments and digital-wallet interfaces are more likely to become part of mainstream banking if supervisors are willing to engage constructively.

For the crypto community in particular, this shift is a reminder that regulation and innovation are not always opposites. When done well, prudential oversight can make it easier for institutional capital to participate in new technologies, because it builds trust that risks are understood and managed.

9. A Turning Point, Not a Finish Line

The Fed’s decision to withdraw its 2023 innovation policy and replace it with a more supportive framework will not overnight transform the U.S. banking sector. Many institutions will remain cautious, and some may choose to watch how early movers fare before committing significant resources.

Yet from a structural perspective, the change marks a turning point in how the central bank talks about technology and experimentation. The message is no longer simply, “stay inside the lines drawn by other agencies.” It is, “bring us your ideas, show us your controls, and we will evaluate them through the lens of safety and soundness.”

For a financial system that is grappling with rapid change — from real-time payments and artificial intelligence to tokenization and new forms of digital money — that shift in tone matters. It suggests that the path forward for banks is not to stand still, but to innovate carefully, transparently and in close dialogue with their supervisors.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment, legal or tax advice. Banking regulation is complex and subject to change. Readers should consult qualified professionals before making financial or compliance decisions.