Inside the World’s Largest Ethereum Treasury: What Bitmine’s Strategy Really Tells Us

Not all Ethereum holders are created equal. At one end of the spectrum are individual users who own a fraction of a coin for experimentation or savings. At the other end sit a small number of entities that treat ETH as a strategic balance-sheet asset, allocating billions over multi-year horizons. Bitmine, helmed by Tom Lee, now belongs firmly in that second group.

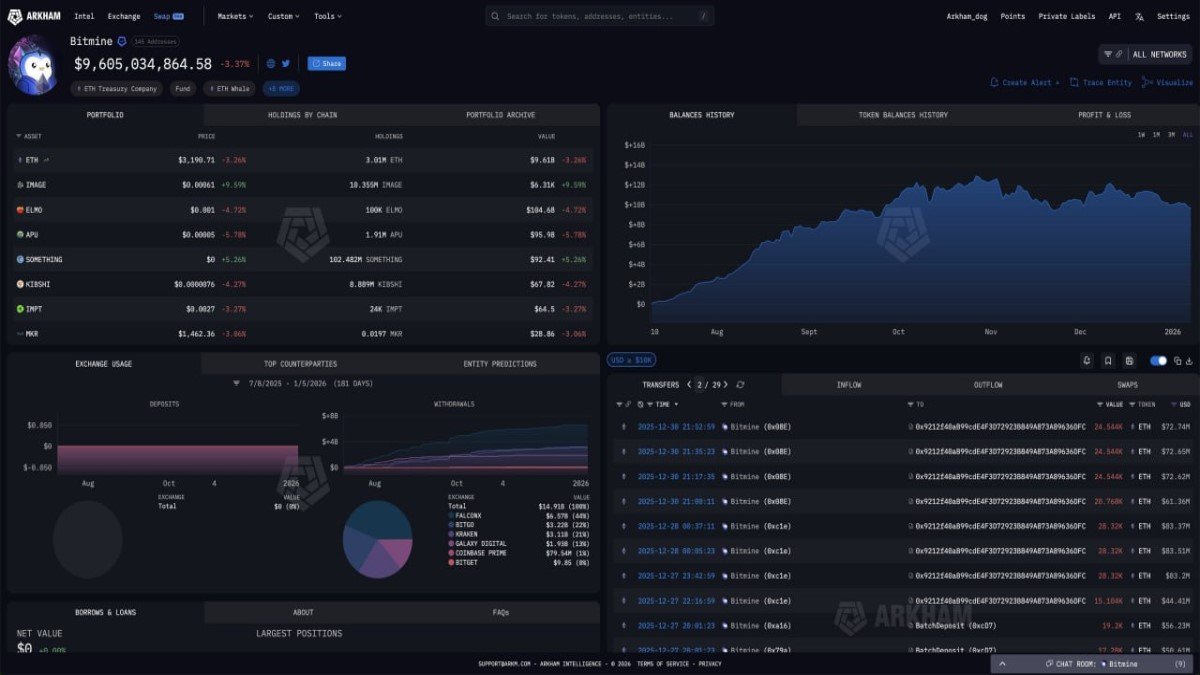

According to recent on-chain observations and treasury commentary, Bitmine has accumulated one of the largest Ethereum positions in existence. The firm’s average purchase price hovers around $4,000 per ETH, and its management team has openly articulated an ambition to control roughly 5% of circulating supply over time. The path to that target has not been smooth: with prices well below the blended entry level, Bitmine is sitting on an estimated unrealised drawdown near 30%, or about $4.5 billion at current marks.

Despite that, the company continues to buy. On 27 November, a wallet associated with BitGo and linked to Bitmine acquired another 14,618 ETH, roughly $44.7 million at recent prices. This purchase came only days after the firm reportedly committed $200 million during a sharp decline. To many observers, the question is obvious: why would a treasury keep increasing exposure into weakness? To answer that, we need to unpack how large institutions think about digital assets, risk and time.

1. Reading the Numbers: Cost Basis, Drawdown and the 5% Ambition

Start with the basic arithmetic. If Bitmine’s blended entry sits near $4,000 and the firm is down roughly 30% on an exposure that now approaches the high single-digit billions, that implies:

- A position sized large enough to matter at the corporate level, not just as a small side allocation.

- A willingness to tolerate severe mark-to-market swings in pursuit of a long-term thesis.

- A clear internal belief that the current price is a snapshot, not a verdict.

The stated objective of eventually holding around 5% of ETH’s circulating supply is even more revealing. This is not the language of a fund that is simply seeking a tactical rebound. It is the language of an owner that wants to be structurally embedded in Ethereum’s monetary base, in a similar way that some institutions historically positioned themselves around gold, sovereign bonds or, more recently, Bitcoin.

A target that high raises legitimate questions about concentration risk and governance, which we will explore later. But it also sheds light on the mindset driving recent purchases: if management believes they are still below their desired long-term allocation, then price weakness becomes a chance to close that gap aggressively, not a reason to retreat.

2. Treasury Play or Trading Bet?

From the outside, it is easy to interpret any large crypto position through the lens of short-term trading: buy low, sell high, repeat. Bitmine’s behaviour suggests a very different framework. Three elements stand out:

• Time horizon. The combination of a multi-billion-dollar position, a clearly stated percentage-of-supply target and continued buying during drawdowns points to a horizon measured in years, not weeks or months.

• Balance-sheet logic. For a corporate treasury, ETH is not just something to flip; it can be framed as a strategic asset that sits alongside cash, bonds or other stores of value in the capital structure.

• Incremental accumulation. Instead of trying to identify a single perfect entry point, the firm appears to be layering in purchases over time, accepting that some tranches will look good in retrospect and others will not.

This does not guarantee success. Long-dated strategies can still fail if the underlying asset underperforms, the thesis proves wrong or external conditions change. But it does change the way we should interpret recent transactions. A treasury that has decided ETH is core to its identity will often be more comfortable buying into drawdowns than an investor whose primary objective is to maximise short-term performance metrics.

3. Why Ethereum? The Thesis Behind Balance-Sheet Exposure

Why might an institution choose Ethereum as a cornerstone asset in the first place? While Bitmine’s internal models are private, the broad contours of a typical ETH thesis at this scale are easy to outline.

First, Ethereum is positioned as a general-purpose settlement layer for digital economies. It hosts decentralised finance protocols, non-fungible token infrastructure, identity tools and an expanding set of enterprise applications. Owning ETH is, in effect, owning a share of the capacity and security budget of that ecosystem.

Second, post-Merge and post-EIP-1559, Ethereum’s monetary profile has changed. The transition to proof-of-stake reduced issuance, while the base-fee burn mechanism destroys a portion of transaction fees in every block. In periods of high activity, net supply growth can slow dramatically and has at times turned negative. For a treasury thinking in decades, this combination of utility demand and potentially constrained net supply is attractive.

Third, ETH is now deeply integrated into institutional infrastructure. Regulated custodians, staking providers, derivatives venues and on-chain analytics all exist at a level of maturity that was absent in earlier cycles. For a firm of Bitmine’s size, the presence of established service partners reduces operational risk around storage, compliance and reporting.

None of this removes uncertainty. Ethereum still faces competition from other smart-contract platforms, regulatory frameworks are still evolving and demand for blockspace can vary significantly through cycles. But the combination of diversified use cases, a predictable monetary mechanism and a robust ecosystem helps explain why a balance sheet might be comfortable treating ETH as more than a passing theme.

4. Living With a 30% Drawdown

An unrealised decline of roughly 30%, on the order of $4.5 billion, is not trivial. For most individuals, that kind of movement would be intolerable. For a well-capitalised institution with clear risk parameters, it can be something different: a stress test of conviction and governance.

Large treasuries typically distinguish between three types of risk:

- Market risk. The day-to-day fluctuation in asset price. This is what shows up in the drawdown figure.

- Liquidity risk. The ability to enter or exit positions without causing excessive slippage or relying on thin markets.

- Fundamental risk. The possibility that the underlying asset’s long-term value proposition deteriorates.

Bitmine’s ongoing accumulation suggests that, in its internal assessment, the third category has not been triggered. In other words, the firm may view the current weakness as a reflection of cyclical market risk, not a breakdown in Ethereum’s fundamentals. That distinction matters. If a thesis fails, adding more exposure can compound the problem. If the thesis remains intact and the treasury has a long-term mandate, incremental purchases at lower prices can reduce the average cost basis over time.

It is also worth noting that unrealised losses are accounting entries, not cash outflows. They affect reported metrics and can influence investor sentiment, but they only crystallise when positions are closed. That does not mean they should be ignored; it does mean that treasuries with stable funding and diversified activities can sometimes accept volatility that would be impossible for more levered players.

5. The Latest Purchases: 14,618 ETH and the Earlier $200 Million Allocation

The recent acquisition of 14,618 ETH through a wallet associated with BitGo, following a much larger $200 million deployment during the prior downturn, fits neatly into this framework. Rather than trying to wait for a perfect bottom, Bitmine appears to be operating with a set of triggers or thresholds: when price, liquidity and internal exposure limits align, the treasury steps in to add.

From a process perspective, this approach has a few advantages:

- Pre-commitment. Decisions are likely guided by pre-defined scenarios instead of improvised reactions to headlines, which can reduce emotional bias.

- Scalability. Breaking a multi-billion-dollar target allocation into staged purchases allows the firm to adapt to new information while still pursuing its long-term goal.

- Operational discipline. Using established custodians and linked wallets provides clear audit trails and can simplify compliance and reporting.

Again, none of this guarantees a positive outcome. If Ethereum’s long-term adoption slows or if macro conditions turn persistently unfavourable, even the most disciplined accumulation can deliver disappointing results. But the pattern is consistent with a deliberate strategy rather than ad-hoc opportunism.

6. Supply, Liquidity and Concentration: System-Level Implications

When a single entity aims to hold up to 5% of a major asset’s circulating supply, the implications extend beyond one balance sheet. There are at least three system-level effects worth highlighting.

Effective float. If Bitmine is truly committed to a long-horizon position, much of its ETH is unlikely to be actively traded in daily markets. That reduces the effective float available to other participants. In theory, lower float can amplify price movements in either direction when demand changes, although the actual impact depends on how other large holders behave.

Perceived endorsement. The presence of a sizable, well-known treasury can influence how other institutions perceive Ethereum. Some may see Bitmine’s exposure as a vote of confidence in ETH’s long-term role; others may worry about concentration and potential future selling pressure. Both reactions are rational and can coexist.

Governance and decentralisation debates. Ethereum’s core protocol is not governed by token-weighted voting in the same way as many application-layer projects. Even so, a holder that large will inevitably wield indirect influence through its public commentary, network relationships and potential participation in staking or ecosystem support. The community will need to balance the benefits of committed institutional capital with ongoing attention to decentralisation.

7. What Smaller Investors Can Learn (Without Copying the Trade)

Most readers will never manage a multibillion-dollar Ethereum treasury. Even so, Bitmine’s approach offers several educational takeaways that can be adapted at very different scales.

• Define your horizon explicitly. Are you thinking in weeks, quarters or years? Bitmine’s behaviour only makes sense when viewed through a multi-year lens. Applying the same tactics with a short-term mindset can be dangerous.

• Separate narrative from process. Public commentary about “buying the dip” is easy. What matters is whether purchases are guided by a coherent plan that includes risk limits and clear reasons to exit if the thesis fails.

• Acknowledge concentration risk. Putting a large share of net worth into a single asset is risky, even if the asset is widely used. Institutional treasuries often mitigate that by pairing strategic positions with diversified operating businesses and other holdings.

• Understand that unrealised losses are inevitable in volatile markets. The question is not whether drawdowns occur, but whether they happen within a range that your financial and psychological situation can tolerate.

Crucially, none of these points imply that individuals should mimic Bitmine’s allocations. The firm’s capital base, regulatory environment and risk tolerance are unique. The lesson is about discipline and clarity of purpose, not about adopting the same exposures.

8. Looking Ahead: Scenarios for a Giant ETH Treasury

Where does this story go next? Several broad scenarios are easy to imagine.

In one, Ethereum’s usage continues to grow across payments, decentralised finance, tokenisation and enterprise applications. Fees remain healthy, net supply growth remains moderate, and ETH’s role as a core settlement asset strengthens. In that world, a large long-term treasury position could eventually recover and perhaps exceed its cost basis by a comfortable margin. Bitmine would look prescient, and other institutions might follow.

In a second scenario, Ethereum persists but faces stronger competition from alternative networks. Activity fragments, fee levels moderate and ETH remains relevant but less dominant. Under those conditions, a concentrated exposure of this size could still work, but the path would be slower and more sensitive to macro cycles.

In a third scenario, unforeseen technological, regulatory or macro shocks weigh on Ethereum’s adoption for an extended period. If that were to happen, even a carefully managed treasury could face difficult choices about whether to maintain, hedge or gradually rebalance exposure. The presence of sophisticated risk management would become even more important than the original accumulation.

The reality will likely involve elements of all three, shifting over time. The key point is that Bitmine’s strategy is a bet not only on price, but on Ethereum’s long-term role in digital finance. That is a different category of decision than simply trying to take advantage of short-term market swings.

9. Conclusion: Conviction, Risk and the Structure of Ownership

Bitmine’s emergence as a leading Ethereum treasury is one of the more striking developments in the current cycle. A multi-billion-dollar position, a clear percentage-of-supply target, continued buying into weakness and a willingness to tolerate deep unrealised drawdowns all point toward a carefully considered, high-conviction strategy rather than a series of isolated trades.

For the Ethereum ecosystem, this raises both opportunities and questions. On the one hand, it signals that major institutions see ETH not just as a speculative instrument but as a long-term strategic asset. On the other, it concentrates ownership in ways that merit ongoing scrutiny and thoughtful discussion about decentralisation, liquidity and governance.

For observers and smaller investors, the most useful takeaway is not whether Bitmine’s specific entry points will prove wise. It is the reminder that serious capital treats digital assets as part of a broader portfolio and policy framework. Clear time horizons, defined risk limits and a willingness to live with volatility are all part of that picture.

Whether Ethereum ultimately justifies this level of conviction will depend on factors no single treasury can control: developer energy, user demand, regulatory clarity and macro conditions. What we can say today is that the structure of ETH ownership is evolving, and entities like Bitmine are helping to shape that evolution in real time.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, investment, legal or tax advice, and it should not be treated as a recommendation to buy, sell or hold Ethereum or any other asset. Market conditions and corporate strategies can change quickly. Readers should conduct their own research and, where appropriate, consult qualified professionals before making decisions related to digital assets or broader financial planning.