Perp DEX: Rebuilding Wall Street On-Chain

For years, the idea that you could reproduce the machinery of global markets inside a few smart contracts sounded ambitious at best. Today, if you open an advanced perpetual futures exchange on-chain, it is hard not to notice how much of the traditional stack has already migrated: order books or virtual AMMs, margin lending, stablecoin settlement, cross-margin portfolios, structured vaults and even options overlays.

These platforms are usually described with a simple label: Perp DEX – decentralized exchanges for perpetual futures. But that phrase understates what is happening. In practice, leading Perp DEXs are evolving into a kind of programmable, borderless 'Wall Street layer' for the internet: a venue where any wallet can access tools that used to be reserved for professional desks and large institutions.

This article looks beyond the usual marketing slogans to unpack three questions:

- What makes a Perp DEX fundamentally different from a centralized broker or a traditional futures exchange?

- How do its economics compare with the cost structure of legacy finance – on fees, settlement, lending and scaling?

- What are the structural opportunities and the real risks as more activity migrates to this on-chain 'financial operating system'?

From Single Product to Integrated Financial Stack

The first generation of decentralized exchanges focused on spot trading. Automated market makers let users swap tokens without an order book, but they did not replace the richer toolbox of Wall Street: margin lending, derivatives, risk-hedging instruments and prime brokerage services.

Perp DEXs change that. A mature platform today often bundles together:

• Perpetual futures with variable funding rates instead of expiry dates, allowing continuous hedging and directional exposure.

• Spot markets and stablecoin pools used for collateral and settlement.

• Lending and borrowing mechanics embedded directly in the margin engine, so every leveraged position is automatically financed through smart contracts rather than a human desk.

• Structured products such as vaults that automate strategies ranging from basis trades to volatility harvesting, often built on top of the core Perp DEX.

• Risk management and liquidation logic encoded in transparent algorithms instead of discretionary policies.

When people say Perp DEXs are becoming the on-chain version of Wall Street, this is what they mean: activities that, in the traditional world, require several institutions – a broker, a clearing house, a prime broker, perhaps an over-the-counter desk – can be orchestrated by composable code sharing a single collateral pool.

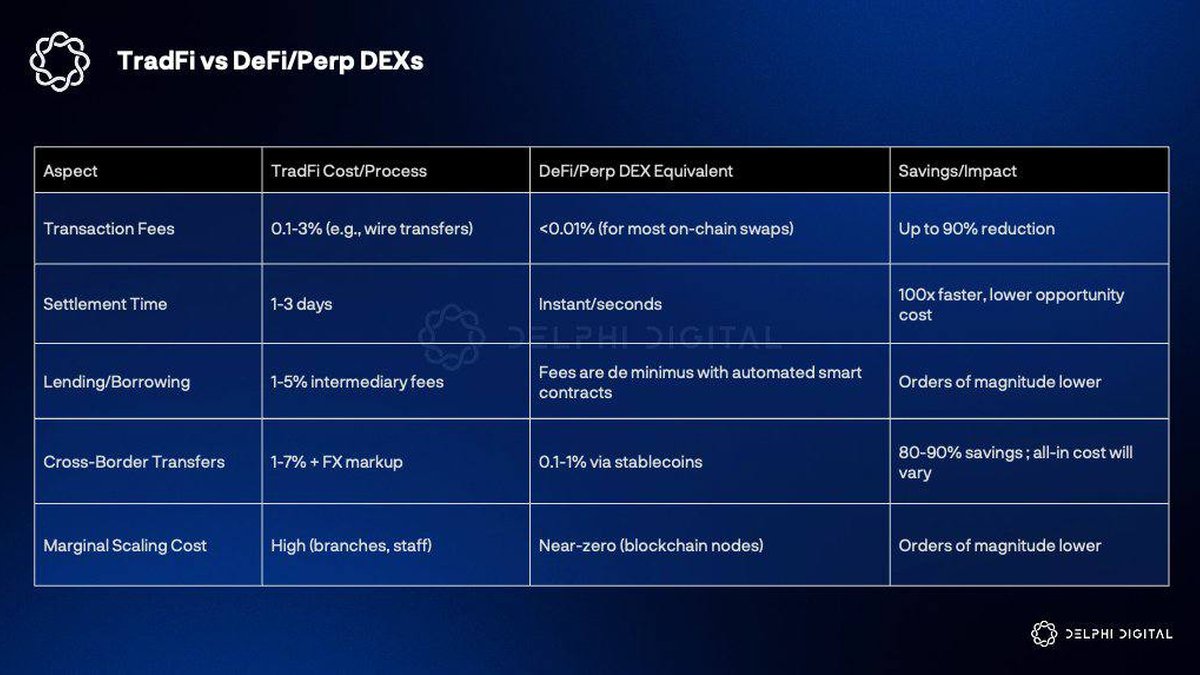

TradFi vs Perp DEX Economics: Where the Friction Goes

A useful way to understand why this matters is to compare typical costs in traditional finance with their on-chain equivalents. A recent breakdown of TradFi vs DeFi/Perp DEXs across key aspects highlights the contrast:

• Transaction fees. Conventional wire transfers or broker trades often cost between 0.1% and 3%, depending on venue and geography. For most on-chain swaps and Perp DEX trades, fees are closer to a few basis points, plus network costs. In benign conditions this can mean fee savings approaching 90%.

• Settlement time. In TradFi, moving cash or securities across institutions typically takes one to three days because of cut-off times, intermediaries and reconciliation steps. On a Perp DEX, settlement is near-instant on the underlying chain: positions update in seconds and balances are immediately usable as collateral elsewhere.

• Lending and borrowing. Banks and brokers usually charge 1–5% above their own funding rate to provide margin loans. In a Perp DEX, the effective financing cost is set algorithmically via funding payments and lending pools, with fees that can be significantly lower because there is no manual middle layer.

• Cross-border flows. International transfers in fiat can cost 1–7% once you include correspondent banking fees and foreign-exchange mark-ups. Stablecoin-based transfers between venues often fall in the 0.1–1% range, depending on slippage and gas.

• Marginal scaling cost. Traditional systems require new branches, staff and infrastructure to serve more users. Public blockchains increase capacity by adding validator or sequencer nodes; once the protocol is running, the cost to support an additional wallet is close to zero.

None of this means that on-chain markets are magically free. Liquidity providers still require compensation, networks can congest, and poorly designed protocols can waste value. But the shape of the cost curve is different. A large share of what would have been operational or overhead expense in TradFi is replaced by one-time software development and ongoing security review.

The Growth Flywheel: Liquidity, Composability and Network Effects

If Perp DEXs were simply cheaper replicas of traditional venues, they would still be interesting. The reason they matter strategically is that they can plug directly into the rest of the on-chain economy.

Consider a basic flywheel:

- Better liquidity and risk management attract traders seeking tight spreads and responsive funding markets.

- Higher volume generates more protocol revenue, which can be used to backstop insurance funds, subsidize new markets or reward long-term contributors.

- Developers build on top, creating vaults, structured notes, automated strategies and user interfaces tailored to different segments.

- End-users access these products through wallets and applications that abstract away the complexity of derivatives, further increasing flow through the core Perp DEX.

Because everything is on-chain, these steps are not separated by paperwork or bilateral negotiation. A new application can integrate with a Perp DEX through code, not legal memoranda, as long as it follows the protocol’s rules. That is very different from asking a traditional exchange for a new product listing or a bespoke margin line.

Over time, the leading Perp DEXs can start to look like hubs in a global financial graph: not just places where people trade, but settlement layers for entire ecosystems of applications. In that sense, they resemble an on-chain Wall Street: an infrastructure core around which other businesses orbit.

Democratizing Access to Advanced Financial Tools

In the legacy system, sophisticated risk management tools are often gated by minimum account sizes, jurisdiction, or institutional relationships. A medium-sized business in an emerging market may struggle to access cost-effective hedging or diversified funding, even though its operations are exposed to currency or commodity swings.

Perp DEXs chip away at that barrier. With nothing more than a wallet and collateral, a user can:

- Hedge directional exposure to an asset they hold elsewhere, by taking an offsetting perpetual position.

- Manage inventory risk if they run a crypto-native business such as a protocol treasury, liquidity-providing strategy or cross-border merchant service.

- Access global dollar liquidity via stablecoins, without relying on local banking infrastructure that may be slow or expensive.

Of course, access is not the same as understanding. Perpetual futures involve leverage, funding dynamics and liquidation thresholds that can magnify both gains and losses. But the fact that these tools are available, transparently documented and executable by code, marks a structural shift. Financial functionality that used to sit behind institutional doors is becoming part of an open, programmable toolkit.

The Architecture of an On-Chain 'Wall Street'

To see how deep the transformation goes, it helps to break down the core building blocks that Perp DEXs assemble.

Unified collateral layer

Traditional brokers often maintain separate margin accounts for different product classes. In contrast, a Perp DEX can treat collateral as a shared pool, with risk parameters tuned per asset. Stablecoins, major cryptoassets and even tokenized real-world instruments can all be posted into the same system, with the risk engine calculating portfolio-level margin requirements.

This design is closer to how sophisticated prime brokers operate – but expressed as transparent formulas and public code rather than customized agreements.

Automated funding and interest rates

In perpetual futures, the funding rate keeps contracts tethered to spot prices by transferring value between long and short positions, typically every few hours. On a Perp DEX, this process is fully automated: the protocol computes the rate and performs the transfers at the smart-contract level. No desk decides when to charge or waive fees.

Additionally, when a Perp DEX integrates lending markets, depositors can earn a share of this funding activity or provide liquidity to the margin system. The interest curve becomes programmable, allowing builders to create products that respond to real-time conditions.

Transparent risk engine

Clearing houses in traditional markets operate according to detailed rulebooks, but their models are not always easy for outsiders to inspect. An on-chain risk engine is, in principle, auditable line by line. Participants can see how maintenance margin is calculated, how liquidation thresholds are set, and what buffers exist to protect the system during stress.

This transparency does not eliminate risk, but it changes its nature. Instead of asking whether a particular firm is acting fairly, users can ask whether the parameters embedded in code match their own tolerance and time horizon.

Challenges: Risk, Regulation and User Protection

It would be misleading to present Perp DEXs as an uncomplicated upgrade over the existing system. As with any powerful tool, there are meaningful challenges.

• Leverage and user education. High leverage can amplify short-term moves. Without clear communication, less experienced users may take on exposures that do not match their goals. Interfaces and educational content need to foreground risk rather than focusing only on potential returns.

• Smart-contract and oracle risk. Because the entire platform runs on code, bugs or design flaws can cause losses if not identified early. Robust auditing, formal verification where possible and conservative parameter choices are critical. Reliable price feeds and resilient infrastructure for index calculations are equally important.

• Regulatory clarity. Different jurisdictions classify derivatives, stablecoins and margin products in different ways. Perp DEXs that want to interact with institutions will need governance frameworks that can incorporate compliance requirements without sacrificing the benefits of open access.

• Liquidity concentration. As top venues accumulate more flow, the ecosystem risks over-reliance on a handful of platforms. Diversity of designs, client segments and collateral types helps reduce this concentration.

These are not reasons to avoid innovation, but they are reminders that on-chain infrastructure is still infrastructure. The same discipline that applies to building bridges or payment networks should apply here: test thoroughly, monitor continuously and assume that stressed conditions will arrive sooner than expected.

How Perp DEXs Reshape the Relationship With Banks

One striking implication of all this is that a growing share of financial activity can, in principle, occur without direct interaction with traditional banks. A business that earns revenue in digital assets can settle invoices, hold reserves in stablecoins, hedge price risk via Perp DEXs and even pay counterparties – all without touching a conventional account, except when converting between fiat and on-chain value.

This does not mean banks disappear. Instead, their role shifts toward gateways: providing regulated access points, custody for institutions that prefer it, and integration between on-chain positions and off-chain obligations like taxes and payroll. In effect, Perp DEXs and surrounding DeFi infrastructure supply the 'engine room' of risk transfer, while banks become high-assurance interfaces between that engine room and the broader economy.

What to Watch in the Next Phase

As Perp DEXs continue to mature, several trends are worth watching from both a market and a policy perspective.

• Deeper integration with real-world assets. As tokenized treasury bills, credit products and equities gain traction, they may be admitted as collateral or even as underlyings for new derivatives. This would bring on-chain markets even closer to the center of global finance.

• Hybrid permission models. Some venues are experimenting with segments where only verified institutions can trade certain products, while the rest of the platform remains open. This could offer a bridge between entirely permissionless environments and regulated demand.

• Advances in risk analytics. On-chain data is uniquely rich. Expect to see dashboards and analytics engines that treat Perp DEXs like transparent laboratories for studying market behavior in real time.

• User-centric safety tools. Features such as default leverage caps, portfolio stress-testing inside the wallet and clearer disclosures can help align the power of perpetual futures with the needs of long-term participants.

Conclusion: A New Financial Operating Layer, Not Just Another Exchange

Perp DEXs began life as a way to trade futures on cryptoassets without relying on centralized intermediaries. They are rapidly becoming something broader: a programmable market infrastructure that unifies trading, lending, risk management and settlement into a single composable layer.

By dramatically lowering transaction and cross-border costs, compressing settlement times from days to seconds and enabling near-zero marginal scaling, these platforms show why on-chain markets can compete with – and in some areas surpass – legacy infrastructure. At the same time, they bring new responsibilities around code safety, leverage management and regulatory cooperation.

Calling Perp DEXs 'Wall Street on-chain' is not about hype; it is a way of recognizing that we are watching an operating system for digital finance come into focus. The open question is how that system will be governed, who will use it, and how well it will balance access, efficiency and protection as it grows.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment, legal or tax advice. Digital assets and derivatives are volatile and involve risk. Always conduct your own research and consult a qualified professional before making financial decisions.