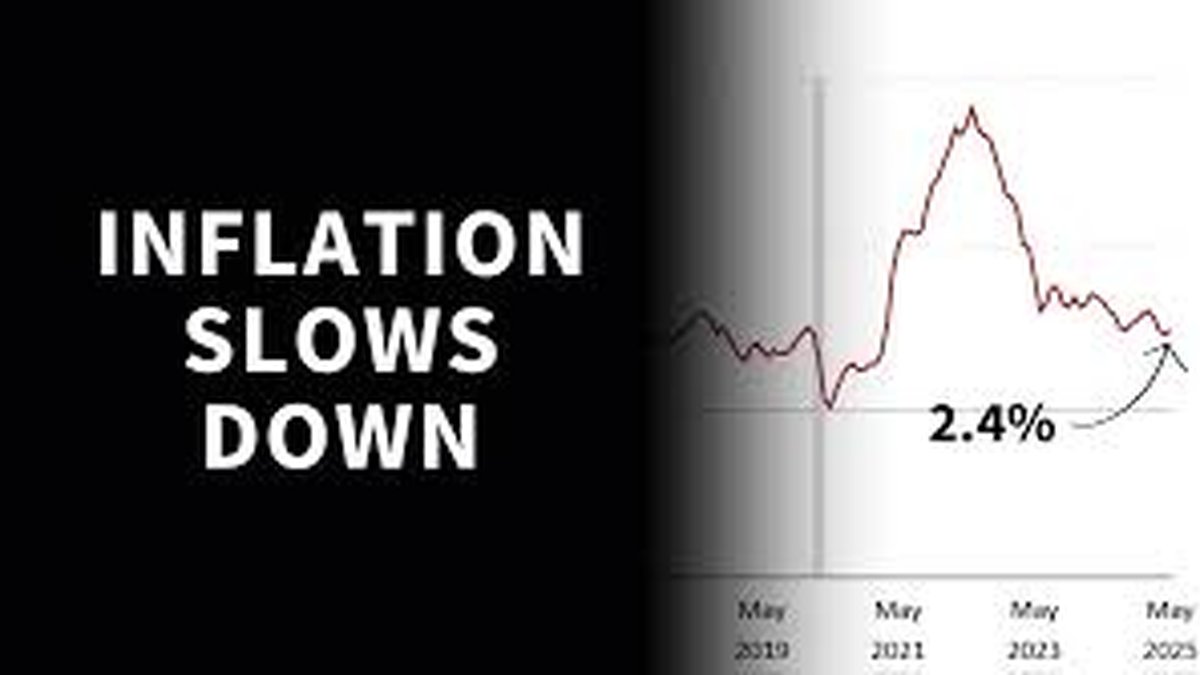

Inflation Eases to 2.6%: What a Cooler CPI Means for the Fed, Markets, and the Path Ahead

The latest U.S. Consumer Price Index (CPI) print showed headline inflation slowing to 2.6% year over year, the lowest level in more than three years. Core inflation also trended lower, reinforcing hopes that the Federal Reserve could begin a gradual rate-cutting cycle in late 2025. Markets greeted the data with a classic risk-on response: Treasury yields dipped across the curve, the dollar softened, and equities advanced. Yet officials at the Fed remain cautious, emphasizing the need for sustained evidence that inflation is on a durable path back to target. This report unpacks what moved, why it matters, and how investors can navigate the next phase.

Inside the CPI: Where the Disinflation Came From

Goods vs. Services

The disinflation mix continues to skew toward goods, where supply chains have normalized and post-pandemic demand has cooled. Apparel, household goods, and consumer electronics saw relatively tame pricing as inventories were rebuilt and freight costs stabilized. On the services side, momentum has eased but remains stickier than goods, reflecting labor-intensive cost structures and ongoing demand for travel, dining, and personal services. The direction of travel is constructive, but services disinflation tends to be gradual and bumpy.

Shelter and the Measurement Lag

Shelter—a large CPI component—continues to moderate with a lag. Private-market measures of new lease growth cooled earlier, but it takes time for those softer prints to filter into the CPI’s owners’ equivalent rent and rent indexes. As older leases roll off and new ones reset at lower increases, shelter inflation should keep drifting down, provided vacancy rates stay stable and construction pipelines add supply.

Core Services ex-Shelter

Policymakers watch core services ex-shelter as a proxy for the wage–price nexus. Recent readings indicate cooling, albeit uneven. Categories tied to discretionary spending (e.g., recreation, hospitality) are more responsive to income growth and labor-market slack; categories tied to healthcare and insurance can move idiosyncratically based on reimbursement schedules or actuarial adjustments. The broad message: pressure is easing but not fully resolved.

Macroeconomic Context: Labor, Wages, and Productivity

Labor-Market Normalization

Hiring has slowed from breakneck post-pandemic rates to a healthier pace. Quit rates have normalized, job openings have drifted lower, and wage growth has cooled from cycle peaks. A labor market that is tight but not overheating reduces the risk of a wage–price spiral and supports the Fed’s confidence in eventual policy normalization.

Real Incomes and Demand

As inflation cools faster than wages in some segments, real income improves. This supports consumption—especially services—even as consumers rotate away from big-ticket goods. The rebalancing helps reduce overheating in interest-rate-sensitive categories while maintaining overall growth momentum.

Productivity and Unit Labor Costs

Improved productivity—helped by digital adoption, automation, and the early benefits of AI-enabled workflows—can absorb wage gains without pushing firms to raise prices. When unit labor costs slow, corporate margin pressure eases, which is disinflationary at the margin and supportive for equities.

Market Reaction and What the Curve is Saying

Rates and the Term Structure

Treasury yields fell, led by the front end as investors marked down the probability of further hikes and nudged forward the timing of the first cut. The belly of the curve (5–7 years) often reflects the market’s best guess of the average policy rate over the next cycle; a soft CPI nudges that path lower, flattening or modestly bull-steepening the curve.

Equities and Factor Leadership

Equities rallied with a rotation toward duration-sensitive segments (technology, software, select internet), while domestically oriented cyclicals also participated on improved soft-landing odds. Value factors held their own where input-cost relief and stable demand support margins (industrial automation, logistics, select staples). Breadth matters: a durable equity upswing is healthier when small and mid caps confirm the move.

Dollar and Commodities

The dollar eased on reduced rate differentials, offering a tailwind to multinational earnings translation. Commodities responded in mixed fashion: growth-sensitive industrial metals found support from better risk sentiment, while energy’s path remains tied to supply dynamics and geopolitics. A cooler inflation impulse lowers the probability of a policy shock that might otherwise choke commodity-sensitive demand.

What it Means for the Fed

Three Conditions for a Pivot

Fed officials have signaled that rate cuts require: (1) consistent disinflation, not a one-off print; (2) evidence that inflation expectations remain anchored; and (3) signs that labor-market balance is improving without cracking. The current CPI checks the direction-of-travel box. To translate into policy action, the data need to repeat—and likely broaden—over several months.

Data Dependence Over Calendar Guidance

Even if markets price cuts for Q4 2025, the Fed’s reaction function remains meeting-by-meeting. Officials will compare incoming CPI/PCE, wages, and activity data against the risk of cutting prematurely (risking a re-acceleration) versus staying tight too long (risking a growth downshift). Communication will likely stress conditionality rather than fixed timelines.

Balance Sheet and Financial Conditions

Beyond policy rates, quantitative tightening (QT) and broader financial conditions (credit spreads, equity levels, mortgage rates) shape the stance of policy. A measured slowing of QT or signaling around reserves could complement rate cuts later, but only if inflation progress looks robust and liquidity conditions warrant adjustment.

Scenario Analysis: Paths From Here

Bull Case: Disinflation Persists, Soft Landing Achieved

Headline and core continue to drift lower, shelter disinflates on schedule, and core services ex-shelter inches down as wage growth cools. The Fed begins a measured cutting cycle in Q4 2025, risk assets extend gains, and rate volatility declines. Multiples expand moderately as earnings hold up and discount-rate uncertainty fades.

Base Case: Choppy Disinflation, Gradual Easing

Progress continues but is punctuated by occasional upside surprises in services or idiosyncratic components (insurance, medical). The Fed waits for a sequence of benign prints before cutting. Markets oscillate within ranges: growth leads when inflation prints cool, cyclicals lead when activity data surprise.

Bear Case: Sticky Services or Energy Shock

Services prices re-accelerate or energy spikes lift headline and expectations. Real yields back up, equities derate, and the Fed stays higher for longer. In this path, the hoped-for Q4 2025 cuts slip or shrink, and recession odds rise.

Risk Dashboard: What Could Derail the Glide Path

Inflation Surprises

Services inflation can prove more persistent due to wage settlements, capacity constraints, or regulatory adjustments (e.g., insurance). A few hot prints can quickly re-price the curve and slam the brakes on multiple expansion.

Growth Downshift

On the other side, a sharp slowdown in hiring, rising delinquencies, or tighter credit conditions could undermine demand. If growth falters while inflation remains above target, policy choices become harder and market volatility rises.

Exogenous Shocks

Geopolitics, supply disruptions, or cyber incidents could alter the inflation/growth mix. Oil spikes, shipping bottlenecks, or sudden import-price shocks would complicate the disinflation narrative.

Investor Playbook: Positioning for a Cooler CPI Regime

For Long-Term Allocators

Maintain diversified exposure with a tilt toward quality growth and free-cash-flow compounders that benefit from lower rate volatility. Balance with cyclicals that gain if the soft landing firms (industrial tech, logistics, travel). Avoid over-concentration in single factors; use macro drawdowns to add selectively.

For Income Investors

Declining rate volatility and credible disinflation support investment-grade credit and dividend growers. Laddered bond portfolios can lock in carry while preserving flexibility if the path to cuts proves uneven.

For Tactical Traders

Into benign prints, call spreads on indices capture upside while containing premium. If services stickiness resurfaces, put spreads provide defined-risk downside. In rates, belly-steepeners may work if the Fed’s first cut nears and the curve normalizes.

Data to Watch Between Now and the Next Fed Decision

Inflation: CPI vs. PCE

The Fed’s preferred gauge is PCE inflation, which differs in weights and methodology. Watch core PCE and supercore (services ex-housing) for confirmation. A synchronized downshift across CPI and PCE would strengthen the case for easing.

Labor: Wages and Job Openings

Average hourly earnings, employment cost index (ECI), and job openings are critical. Slower wage growth with stable employment is the ideal combination for disinflation without recession.

Activity: ISM/PMIs and Consumption

Services PMIs, retail sales, and card-spend trackers will show whether consumers keep spending as real incomes improve. A resilient demand backdrop allows the Fed to cut because it can, not because it must.

Frequently Asked Questions

Does 2.6% headline inflation guarantee rate cuts? No. It improves odds, but the Fed needs a pattern of benign data and confidence that inflation expectations are anchored.

Why do markets react so strongly to one report? CPI updates the market’s estimate of future real rates and the timing/pace of policy moves. Even one data point can shift probabilities enough to move prices.

What if shelter doesn’t cool as expected? Disinflation could stall. The Fed would look for broader services relief or slower wage growth before considering cuts.

How do lower yields help equities? Lower discount rates raise the present value of future cash flows, especially for long-duration assets like tech and high-growth software.

Bottom Line

The step down in CPI to 2.6% YoY is a meaningful milestone on the road back to price stability. Markets have responded by leaning into a soft-landing narrative—lower yields, firmer equities, and a weaker dollar. But for the Fed, one cool print is necessary, not sufficient. The bar for a pivot includes repeated confirmation across inflation, wages, and activity. For investors, the playbook is to respect the disinflation trend while staying humble about the path: emphasize quality, duration-sensitive winners, and defined-risk tactics in case services stickiness or shocks challenge today’s optimism. If the cooling persists, a gradual easing cycle in late 2025 becomes the base case, and risk assets can grind higher on a more stable macro foundation.